Navigating the complexities of future healthcare needs can be daunting, but understanding long term care insurance offers a critical path to peace of mind. This comprehensive guide will equip you with the knowledge to make informed decisions about protecting your assets and ensuring quality care as you age. We’ll break down everything from policy types to costs, empowering you to secure your financial future and that of your loved ones.

What is Long-Term Care Insurance and Why You Need It

Long term care insurance is a specialized type of coverage designed to help pay for the costs associated with long-term care services. These services are typically needed when you can no longer perform daily activities on your own due to aging, illness, or injury. This includes assistance with bathing, dressing, eating, continence, toileting, and transferring.

Why does this matter in real life? Traditional health insurance, including Medicare, generally does not cover long-term care services like assistance with daily activities. Medicare primarily covers skilled nursing care or short-term rehabilitation. Without a plan, the financial burden of extended care can quickly deplete savings and impact family members.

Imagine a scenario where a loved one develops a chronic condition requiring daily assistance at home or in a facility. In a typical month, care costs could range from several thousand dollars for in-home care to upwards of $8,000-$10,000 for a nursing home. Without long-term care insurance, these expenses would fall entirely on your family, potentially leading to financial hardship.

Traditional vs. Hybrid Policies

When considering long term care insurance, you’ll encounter two main types: traditional and hybrid policies. Understanding the differences is crucial for selecting the right fit for your needs and financial situation.

- Traditional Long-Term Care Policies: These policies focus solely on covering long-term care costs. You pay premiums, and if you need care, the policy pays out. If you never need long-term care, the premiums paid are typically not returned. Why this matters: They can offer extensive coverage for a lower initial premium if purchased at a younger age.

- Hybrid Long-Term Care Policies (Asset-Based): These combine long-term care coverage with a life insurance policy or an annuity. If you need long-term care, the policy pays out for those services. If you don’t use the long-term care benefits, a death benefit is paid to your beneficiaries, or a cash value is available. Why this matters: They offer a “use it or lose it” solution, as there’s usually a payout regardless of whether care is needed, providing more flexibility and certainty.

The Rising Cost of Long-Term Care

The cost of long-term care services continues to climb significantly each year. This makes planning ahead with a strategy like long term care insurance incredibly important. Understanding these costs is vital to prevent them from becoming a financial crisis later in life.

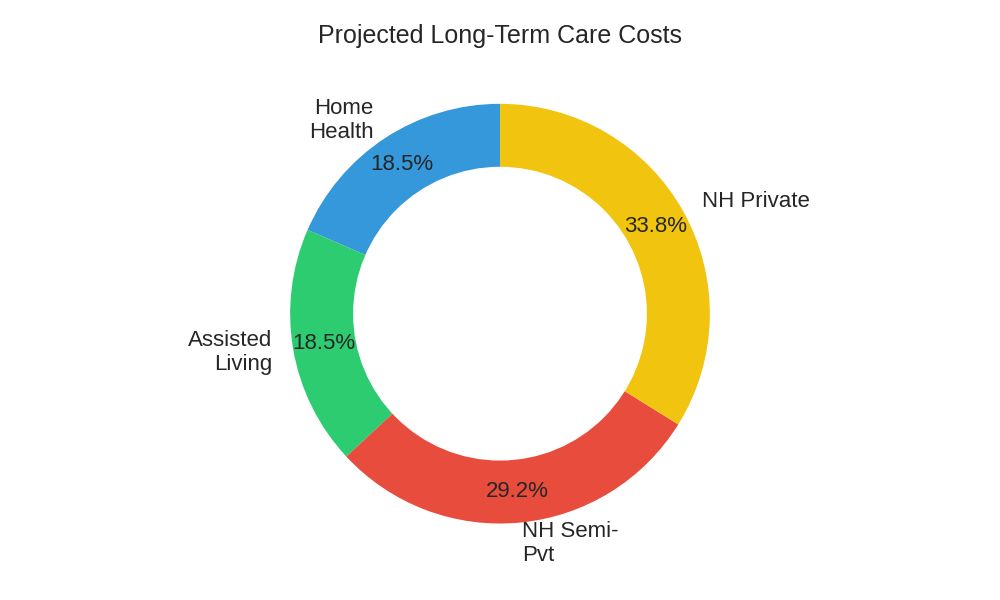

Why does this matter in real life? The average cost of care can quickly become unaffordable for many families. For example, a semi-private room in a nursing home can cost between $90,000 and $120,000 per year, while assisted living facilities typically range from $50,000 to $70,000 annually. In-home care, depending on the number of hours, can also accumulate to similar figures.

Government programs like Medicare do not cover most long-term care needs, and Medicaid only kicks in once a person has depleted nearly all their assets. This leaves most individuals and families to bear the burden of these costs themselves. Protecting your assets from these potentially devastating expenses is a primary benefit of having a dedicated policy.

| Type of Care | Estimated Annual Cost Range (Today) | Projected Annual Cost (20 Years Later) |

|---|---|---|

| Home Health Aide (44 hrs/week) | $55,000 – $65,000 | $110,000 – $130,000 |

| Assisted Living Facility (Private Room) | $50,000 – $70,000 | $100,000 – $140,000 |

| Nursing Home (Semi-Private Room) | $90,000 – $100,000 | $180,000 – $200,000 |

| Nursing Home (Private Room) | $100,000 – $120,000 | $200,000 – $240,000 |

This table illustrates how quickly long-term care costs can escalate over time due to inflation. Planning for these future expenses is a crucial step in comprehensive financial planning.

Key Features to Look for in a Policy

Choosing a long-term care insurance policy involves understanding several key features that directly impact your coverage and out-of-pocket costs. These features define how and when your policy will pay for services.

- Daily or Monthly Benefit Amount: This is the maximum amount your policy will pay for care each day or month. Why this matters: A higher benefit means more coverage, but also higher premiums. Consider the average costs in your area.

- Benefit Period: This refers to the length of time the policy will pay for care (e.g., 2 years, 3 years, 5 years, or lifetime). Why this matters: A longer benefit period provides more protection against extended care needs, but comes at a greater cost.

- Elimination Period (Waiting Period): This is the number of days you must pay for care out-of-pocket before your policy begins to pay. Common periods are 30, 60, or 90 days. Why this matters: A shorter elimination period means the policy starts paying sooner, reducing your immediate costs, but increases premiums.

- Inflation Protection: This vital feature increases your daily benefit over time to keep pace with the rising cost of care. Why this matters: Without inflation protection, a policy purchased today might only cover a fraction of care costs two decades from now. This is a critical component for long-term planning.

- Types of Care Covered: Ensure the policy covers the types of care you might need, such as home health care, adult daycare, assisted living, and nursing home care. Why this matters: Broad coverage provides flexibility in where and how you receive care, aligning with your preferences.

How to Calculate Your Potential Long-Term Care Needs

Estimating your future long-term care needs can help you determine the right amount of coverage. This isn’t a precise science, but a practical estimation process. Start by considering the potential duration of care you might need and the daily cost of care in your area.

First, estimate how many years you might need care. For instance, you might assume you’ll need care for 2-5 years. Next, research the current average daily cost of care services in your specific region for home care, assisted living, or nursing home facilities. You can find this data from state health departments or national organizations.

Multiply the estimated daily cost by the number of days in a year (365). This gives you an annual cost. Then, multiply this annual cost by your estimated number of years of care. Finally, consider adding an inflation factor, typically around 3-5% per year, to project what those costs might be in the future when you actually need care. This calculation will give you a rough total you might need to cover, helping you select an appropriate policy benefit amount.

Long Term Care Insurance Peace of Mind for Tomorrow

Who Should Consider Long-Term Care Insurance?

Long-term care insurance isn’t for everyone, but certain individuals stand to benefit significantly. The decision often hinges on your age, health, and financial situation. It’s about protecting assets and maintaining autonomy in care decisions.

Imagine two individuals, Sarah and Mark. Sarah is in her early 50s, in good health, and has a substantial retirement nest egg she wants to protect for her children. For Sarah, purchasing a policy now makes sense; premiums are lower, and she’s likely to qualify for coverage. This ensures her savings aren’t depleted by potential future care costs. Mark, however, is in his late 70s with several pre-existing conditions and limited assets. For Mark, a policy might be too expensive or unobtainable, and he might instead rely on Medicaid or family support.

Generally, those who should consider it are: individuals between 50 and 65 years old, those with significant assets to protect, and individuals with a family history of chronic illness or conditions that often require long-term care. It’s a proactive measure to safeguard your future well-being and financial legacy.

The Application Process: What to Expect

Applying for long-term care insurance involves a thorough review of your health and financial situation. Insurers want to assess their risk, so be prepared for a detailed process. Transparency is key to a smooth application.

- Application Form: You’ll start by filling out a comprehensive application detailing your personal information, health history, and sometimes financial details.

- Medical Underwriting: This is a crucial step where the insurer evaluates your health. It typically involves answering detailed health questions, providing access to your medical records, and possibly undergoing a cognitive or functional assessment over the phone or in person.

- Financial Assessment: For some policies, especially those with larger benefit amounts, insurers may assess your financial stability to ensure you can afford the premiums over the long term.

- Offer and Acceptance: If approved, the insurer will offer you a policy with specific terms and premiums. You’ll then review and decide whether to accept the offer.

Making the Right Choice: Steps to Take

Choosing the right long-term care insurance policy requires careful consideration and research. This decision can have long-lasting financial implications, so taking a structured approach is essential.

- Assess Your Needs: Start by evaluating your personal health, family history, and financial situation. Consider how much care you might need and for how long.

- Research Policy Types: Understand the differences between traditional and hybrid policies, and which aligns best with your financial goals.

- Compare Insurers and Policies: Get quotes from multiple reputable insurers. Compare daily benefit amounts, elimination periods, inflation protection options, and the types of care covered. The National Association of Insurance Commissioners (NAIC) provides valuable resources to help consumers understand insurance products and compare options; you can learn more at NAIC.org.

- Understand the Costs: Premiums can vary significantly based on your age, health, the amount of coverage, and features like inflation protection. Consider how premiums fit into your long-term budget.

- Seek Professional Advice: Consult with a qualified financial advisor or insurance specialist who can help you navigate the complexities and tailor a plan to your specific circumstances. For guidance on finding a professional, resources like the Financial Planning Association can be helpful; explore more at FinancialPlanningAssociation.org.

- Read the Fine Print: Carefully review the policy document for exclusions, limitations, and terms for increasing premiums. Understanding all aspects of your contract is vital. For general consumer protection information, consider visiting USA.gov.

Frequently Asked Questions (FAQ)

- Q: Does Medicare cover long-term care?A: Generally, no. Medicare covers skilled nursing care and rehabilitation for a limited time, but it does not cover ongoing custodial care for daily living activities.

- Q: Is long-term care insurance tax-deductible?A: In some cases, premiums for qualified long-term care insurance policies may be partially tax-deductible as medical expenses, subject to IRS limits based on age. Consult a tax professional for personalized advice.

- Q: Can I afford long-term care insurance?A: Premiums vary widely based on age, health, and policy features. It’s crucial to get multiple quotes and compare options. Consider it an investment in protecting your future financial security.

- Q: What if I never need long-term care?A: With traditional policies, if you never need care, the premiums paid are generally not returned. Hybrid policies, however, offer a death benefit or cash value if long-term care benefits are not used.

- Q: When is the best time to buy a policy?A: Generally, the earlier you buy (often in your 50s), the lower your premiums will be, and the easier it is to qualify for coverage. Waiting until you are older or have health issues can make policies much more expensive or even unobtainable.

Conclusion

Preparing for future long-term care needs is a crucial step in comprehensive financial planning. Understanding the nuances of long term care insurance empowers you to protect your assets, ensure access to quality care, and alleviate potential burdens on your loved ones. While the decision to purchase a policy is personal, the peace of mind it offers can be invaluable.

Don’t leave your future care to chance. Take the initiative to explore your options, compare policies, and consult with a trusted financial advisor today. Secure your tomorrow by planning today.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.