In today’s financial landscape, letting your hard-earned cash sit idly in a traditional savings account is akin to leaving money on the table. For savvy savers, an online banking high yield savings account presents a compelling alternative, offering significantly higher interest rates than brick-and-mortar banks. This comprehensive guide will explain everything you need to know about harnessing the power of an online banking high yield savings account to maximize your earnings and achieve your financial goals faster.

Simply put, an online banking high yield savings account is a savings account offered by online-only financial institutions that pays a much higher interest rate, known as Annual Percentage Yield (APY), on your deposited funds compared to conventional savings accounts. These accounts typically boast fewer fees and greater flexibility, making them an excellent choice for building emergency funds, saving for a down payment, or reaching any significant savings milestone. Let’s dive deeper into how this powerful tool can transform your savings strategy.

What is an Online Banking High Yield Savings Account?

An online banking high yield savings account is a type of savings account managed entirely online, without physical branch locations. This allows these institutions to operate with lower overhead costs. As a result, they can pass these savings on to their customers in the form of significantly higher interest rates, often referred to as a superior Annual Percentage Yield (APY).

Why does this matter in real life? Imagine you have $10,000 in savings. In a traditional bank, you might earn a meager 0.01% APY, yielding just $1 in interest after a year. With an online banking high yield savings account offering, for example, 4.50% APY, that same $10,000 could earn you $450 in interest over the same period. This difference can substantially accelerate your savings growth.

Understanding Annual Percentage Yield (APY)

APY stands for Annual Percentage Yield, and it represents the total amount of interest you’ll earn on your savings over one year, taking into account the effect of compounding interest. Compounding means you earn interest not only on your initial deposit but also on the interest you’ve already accumulated. This is why APY is a crucial metric when comparing savings accounts.

Why does this matter in real life? A higher APY means your money grows faster. It shows you the true earning power of your savings account, allowing you to make an informed decision based on the actual return you can expect.

Key Benefits of an Online High-Yield Savings Account

Beyond the attractive interest rates, online high-yield savings accounts offer several other advantages that make them a smart choice for modern savers.

Higher Interest Rates

As discussed, the primary draw of these accounts is their superior interest rates. Online banks don’t have the expenses associated with maintaining physical branches, like rent, utilities, and a large branch staff. This operational efficiency allows them to offer more competitive rates to attract and retain customers.

Why does this matter in real life? Your money works harder for you. Instead of inflation eroding your purchasing power in a low-interest account, a high-yield account helps your savings grow, keeping pace or even exceeding inflation.

Lower Fees

Many online banking high yield savings accounts come with minimal to no monthly maintenance fees, overdraft fees, or minimum balance requirements. This contrasts sharply with some traditional banks that may charge fees if certain conditions aren’t met.

Why does this matter in real life? Every dollar saved on fees is a dollar that stays in your account, earning interest. This maximizes your overall return and prevents unnecessary deductions from your hard-earned savings.

Convenience and Accessibility

With an online account, you can manage your money 24/7 from anywhere with an internet connection. Most online banks offer robust mobile apps, allowing you to check balances, transfer funds, and deposit checks directly from your smartphone.

Why does this matter in real life? Imagine you’re traveling or working odd hours. You don’t need to rush to a bank branch before it closes. The flexibility of online access ensures you’re always in control of your finances, fitting seamlessly into your busy life.

FDIC Insurance Protection

One common concern about online-only banks is security. Rest assured, legitimate online banking high yield savings accounts are insured by the Federal Deposit Insurance Corporation (FDIC) for up to $250,000 per depositor, per insured bank, for each account ownership category. This is the same protection offered by traditional brick-and-mortar banks.

Why does this matter in real life? Your deposits are safe and secure. Even if the online bank were to fail, the FDIC would protect your money up to the insurance limit. You can learn more about this protection at the FDIC website.

How to Choose the Best Online Banking High Yield Savings Account

Selecting the right online savings account involves more than just finding the highest APY. Here’s a step-by-step approach to finding the best fit for your financial needs:

- Compare APY Rates: Always start by comparing the Annual Percentage Yields offered by different institutions. Even a small difference in APY can lead to significant earnings over time.

- Scrutinize Fees and Requirements: Look for accounts with no monthly maintenance fees and reasonable, if any, minimum balance requirements to earn the advertised APY.

- Check Deposit and Withdrawal Options: Ensure the bank offers convenient ways to deposit money (e.g., electronic transfers, mobile check deposit) and withdraw funds (e.g., ACH transfers to linked accounts).

- Evaluate Customer Service: While online, you’ll still need support sometimes. Look for banks with strong customer service ratings, available via phone, chat, or email during convenient hours.

- Review Mobile App Experience: Test drive their mobile app if possible, or read reviews. A user-friendly app makes managing your money much easier on the go.

Why does this matter in real life? Imagine you’ve narrowed it down to two accounts. One has a slightly higher APY but charges a $5 monthly fee if your balance dips below $1,000. If you anticipate your balance might fluctuate, the account with a slightly lower APY but no fees could actually save you more money in the long run.

Practical “How to Calculate” Your Potential Earnings

Understanding how much you can potentially earn from an online banking high yield savings account is simpler than you might think, even without complex formulas. Let’s break it down.

First, know your Annual Percentage Yield (APY). Let’s say it’s 4.50%. This means you’ll earn 4.50% on your money over a full year, assuming interest compounds.

To estimate your monthly earnings, you can take your current balance, multiply it by the APY, and then divide by 12. So, if you have $10,000 and the APY is 4.50% (or 0.045 as a decimal), you’d calculate: $10,000 x 0.045 = $450. Then, $450 / 12 = $37.50 in estimated interest for that month.

However, because interest compounds (you earn interest on your interest), your actual earnings will be slightly higher over the year. For example, if you add money regularly, your monthly interest calculation will be on a growing balance.

For more precise calculations that factor in compounding and regular deposits, you can use online calculators. These tools help visualize your growth over time.

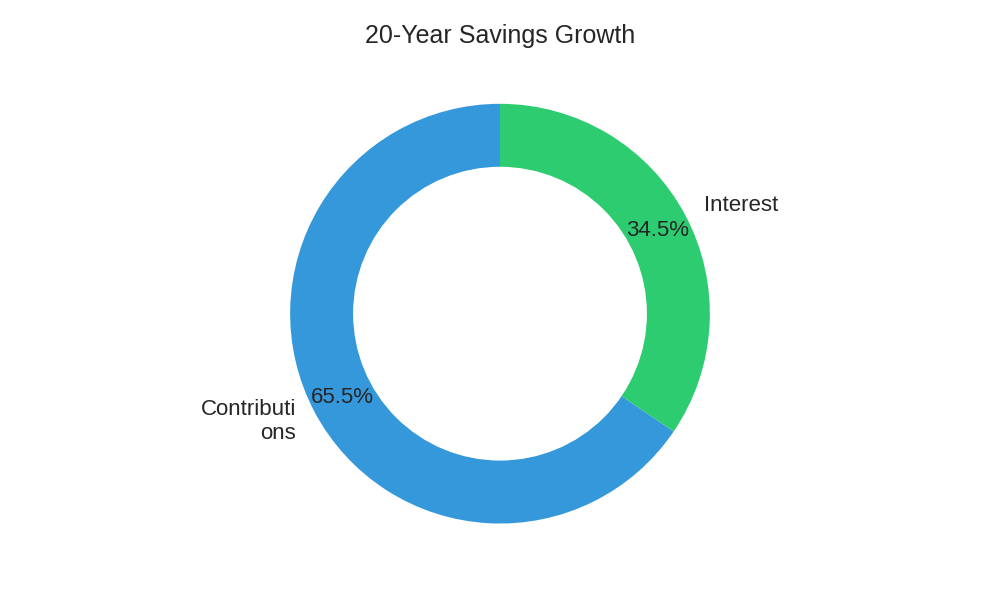

High Yield Savings Growth

To illustrate the power of compounding and consistent contributions, consider this scenario:

| Year | Initial Deposit: $5,000 | Monthly Contribution: $150 | Estimated APY: 4.25% |

|---|---|---|---|

| Year | Total Contributions | Estimated Interest Earned | Total Balance (Approx.) |

| 1 | $6,800 | $265 – $300 | $7,065 – $7,100 |

| 5 | $14,000 | $1,800 – $2,200 | $15,800 – $16,200 |

| 10 | $23,000 | $5,500 – $6,500 | $28,500 – $29,500 |

| 20 | $38,000 | $20,000 – $23,000 | $58,000 – $61,000 |

Why does this matter in real life? This table clearly demonstrates that even modest, consistent contributions, combined with a good APY, can lead to substantial wealth accumulation over the long term, thanks to the power of compound interest.

Common Misconceptions and Smart Strategies

While the benefits are clear, some misconceptions still circulate about online banking high yield savings accounts. Addressing these can help you make the most of your money.

- Myth: Online banks are less secure. Reality: As mentioned, most reputable online banks are FDIC-insured, offering the same level of protection as traditional banks. They also employ advanced encryption and security measures.

- Myth: You can’t access your money quickly. Reality: While instant cash withdrawals aren’t typically available at an ATM linked directly to your savings, transferring funds to a linked checking account at another bank usually takes 1-3 business days. For faster access, some online banks offer debit cards for their savings accounts or instant transfer options to their own checking accounts.

- Strategy: Automate your savings. Set up recurring transfers from your checking account to your high-yield savings account. This makes saving effortless and consistent, ensuring you continually benefit from compounding.

- Strategy: Segment your savings goals. Consider opening multiple high-yield savings accounts for different goals (e.g., “Emergency Fund,” “Vacation Fund,” “Down Payment Fund”). This helps you stay organized and motivated.

Why do these strategies matter in real life? Automation removes the effort from saving, while segmentation gives each dollar a purpose. Both approaches help you build financial discipline and achieve specific goals more effectively.

Frequently Asked Questions (FAQ)

Are online banks safe?

- Yes, generally. Most reputable online banks offering an online banking high yield savings account are FDIC-insured, meaning your deposits are protected up to $250,000 per depositor. They also use robust cybersecurity measures. Always verify a bank’s FDIC insurance status. For more information on protecting your finances, consult resources like the Consumer Financial Protection Bureau.

How often does interest compound?

- Interest typically compounds daily or monthly, meaning your earnings are added to your principal more frequently. This allows you to start earning interest on your interest sooner, leading to greater overall growth.

Are there withdrawal limits?

- Yes, federal regulations (Regulation D) historically limited certain withdrawals and transfers from savings accounts to six per month. While Regulation D was suspended during the pandemic, banks may still impose their own limits. Always check a bank’s specific terms and conditions.

What about taxes on interest earned?

- Interest earned from savings accounts is considered taxable income by the IRS. Your bank will issue a 1099-INT form if you earn more than $10 in interest in a year. Be sure to report this income when filing your taxes. For detailed tax guidance, you can visit the IRS website.

Conclusion

Choosing an online banking high yield savings account is a smart financial move for anyone looking to maximize their savings potential. With higher interest rates, lower fees, enhanced convenience, and FDIC protection, these accounts offer a powerful tool to grow your wealth more efficiently than traditional options.

Don’t let your money sit idly by. Take control of your financial future by exploring the benefits of a high-yield savings account today. Start researching, compare rates, and open an account to begin earning more on your cash.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.