Navigating the complexities of healthcare can be daunting. In a world where health is paramount, understanding your options for medical care is crucial. This comprehensive guide will demystify private medical insurance, explaining its nuances and empowering you to make informed decisions about your well-being. Private medical insurance offers a way to access healthcare services outside of public systems, providing more control over your treatment journey.

At its core, private medical insurance (PMI) is a policy that covers the costs of private healthcare treatment for acute conditions that develop after your policy starts. It can offer quicker access to specialists, a wider choice of hospitals, and more flexible appointment times compared to public healthcare systems. This guide will walk you through what it is, its benefits, how to choose a plan, and what costs to expect.

What is Private Medical Insurance?

Private medical insurance, often simply called health insurance, is a contract between you and an insurance company. In exchange for regular payments, known as premiums, the insurer agrees to pay for specified private medical treatments if you get sick or injured. It typically covers a range of services from consultations and diagnostic tests to surgeries and hospital stays.

Why does this matter in real life? Imagine you develop a sudden knee pain. With public healthcare, you might face a significant waiting list for an MRI scan and then for a specialist consultation. With private medical insurance, you could potentially see a consultant and get diagnostic tests much faster, leading to a quicker diagnosis and treatment plan. This speed can be critical for both peace of mind and recovery.

Key Benefits of Private Medical Insurance

Choosing private medical insurance offers several distinct advantages that can significantly enhance your healthcare experience. These benefits often address common concerns about public health systems, such as waiting times and choice.

- Faster Access to Treatment: One of the most compelling reasons for private medical insurance is the reduced waiting times for consultations, diagnostic tests, and treatments. This means you can often get seen by specialists much sooner. Why this matters: Early diagnosis and treatment can lead to better outcomes and less time spent in discomfort or worry.

- Choice of Specialists and Hospitals: You typically have the flexibility to choose your consultant and the hospital where you receive treatment, often from an approved network. Why this matters: This allows you to select a doctor known for their expertise in a specific area or a hospital with facilities that suit your needs.

- Comfort and Privacy: Private hospitals often offer a more comfortable environment, including private rooms with en-suite bathrooms. Why this matters: A peaceful and private recovery environment can contribute significantly to patient well-being and recovery.

- Flexible Appointments: Private healthcare often provides more flexibility in scheduling appointments to fit your personal or work commitments. Why this matters: This convenience can reduce stress and disruption to your daily life during periods of illness.

- Access to Advanced Treatments: Some policies may offer access to drugs and treatments not yet readily available on public health systems. Why this matters: This can provide options for conditions where standard treatments have been exhausted or are less effective.

For more insights on healthcare options and consumer rights, you can visit official government resources like USA.gov.

Understanding Types of Private Medical Insurance Plans

Private medical insurance plans come in various forms, each offering different levels of coverage and flexibility. Understanding these distinctions is key to finding a plan that matches your needs and budget.

Common types include:

- Comprehensive Plans: These offer the broadest coverage, including inpatient treatment (hospital stays, surgeries), outpatient consultations, diagnostic tests, and sometimes even complementary therapies.

- Inpatient Only Plans: These are more basic and cover treatment that requires an overnight stay in a hospital. They typically exclude outpatient care like specialist consultations or diagnostic tests performed without admission.

- Outpatient Only Plans: Less common as standalone policies, these cover services that don’t require an overnight hospital stay, such as specialist appointments, scans, and therapies.

- Cash Plans: These aren’t traditional insurance but pay out a fixed amount of cash towards routine healthcare costs like dental, optical, or physiotherapy, regardless of whether you use public or private services.

How to Choose the Right Plan: Factors to Consider

Selecting the best private medical insurance plan requires careful consideration of several factors. Your personal health needs, financial situation, and lifestyle all play a role.

- Coverage Level: Decide what you want covered. Do you need extensive cover for all eventualities, or are you comfortable with a basic plan that only covers inpatient care? This matters because a higher level of coverage means a higher premium, but potentially lower out-of-pocket costs later.

- Deductible (or Excess): This is the amount you agree to pay towards your treatment costs before your insurer starts paying. For example, if your deductible is $1,000, you would pay the first $1,000 of your medical bills in a policy year. Why this matters: A higher deductible usually means lower monthly premiums, but you’ll pay more out-of-pocket if you make a claim.

- Co-payment: Some policies require you to pay a percentage of the treatment cost, known as a co-payment, even after meeting your deductible. Why this matters: This further reduces your premium but means you’ll still have ongoing costs during treatment.

- Hospital Network: Most insurers have a network of approved hospitals and clinics. Ensure your preferred facilities or specialists are part of the plan’s network. Why this matters: If you go outside the network, your treatment might not be covered, or you’ll pay more.

- Pre-existing Conditions: Policies often have specific rules regarding conditions you had before taking out the insurance. Always disclose these truthfully. Why this matters: Undisclosed pre-existing conditions can invalidate your policy or lead to claims being denied.

Calculating Your Private Medical Insurance Costs

The cost of private medical insurance, your premiums, can vary significantly based on several factors. It’s not a one-size-fits-all expense, and understanding what influences the price can help you budget effectively.

Key factors that influence your premiums include:

- Age: Generally, the older you are, the higher your premiums. This is because the risk of needing medical care typically increases with age.

- Health Status: Your current health and medical history, including any pre-existing conditions, will impact the cost.

- Location: Healthcare costs vary by region, and your geographical location can affect your premium. For example, policies in major metropolitan areas might be more expensive due to higher local medical costs.

- Chosen Plan: The level of coverage, deductible, and additional benefits you select will directly influence the premium. More comprehensive plans are more expensive.

- Lifestyle: Factors like smoking habits can also affect your premium.

How to Estimate Your Potential Costs

While exact figures require a personalized quote, you can estimate potential costs by considering the factors above. Think about your likely usage, your comfort level with a deductible, and the breadth of coverage you desire.

To get a clear picture of what private medical insurance might cost you, it’s essential to compare quotes based on your specific needs and situation. Online tools and direct inquiries with providers can help you navigate the options and determine an estimated premium.

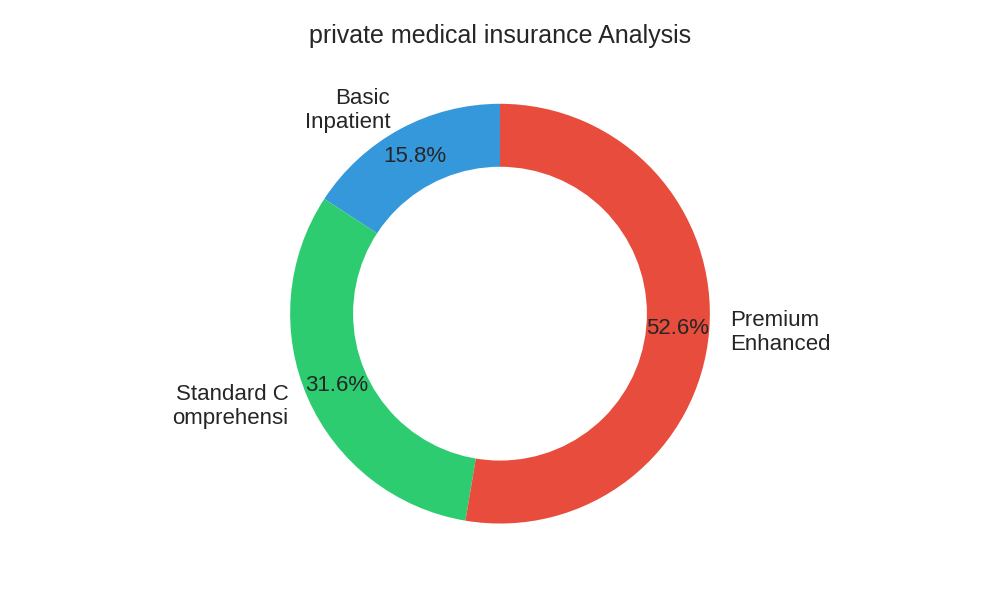

Private Medical Insurance Cost Estimator

| Plan Type | Estimated Monthly Premium (Range) | Typical Deductible (Range) | Estimated Annual Out-of-Pocket Max (Range) |

|---|---|---|---|

| Basic Inpatient Only | $150 – $300 | $1,000 – $3,000 | $3,000 – $6,000 |

| Standard Comprehensive | $300 – $600 | $500 – $2,000 | $5,000 – $10,000 |

| Premium Enhanced (Low Deductible) | $500 – $900 | $0 – $500 | $2,000 – $5,000 |

This table provides illustrative ranges. Actual costs will depend on your personal circumstances and the insurer. For more information on health insurance costs and trends, reputable financial news sources like Forbes often provide in-depth analysis.

Navigating Pre-existing Conditions and Waiting Periods

When considering private medical insurance, two terms you’ll frequently encounter are pre-existing conditions and waiting periods. Understanding these is crucial for managing your expectations regarding coverage.

A pre-existing condition is any illness, injury, or symptom you had or received advice/treatment for before starting your policy. Most insurers have specific underwriting rules for these. For instance, if you had asthma symptoms and treatments before purchasing the policy, your insurer might exclude any future asthma-related claims for a certain period, or entirely. Why this matters: It directly impacts what conditions your policy will cover from day one, so always be honest about your medical history.

Waiting periods are set times after your policy starts during which you cannot claim for certain conditions or treatments. These periods are designed to prevent people from buying insurance only when they know they need immediate expensive treatment. For example, a policy might have a 3-month waiting period for diagnostic tests or a 12-month waiting period for certain elective surgeries. Why this matters: You need to be aware that even if you’ve paid your premiums, you might not be able to claim for immediate needs related to specific conditions until the waiting period has passed.

Frequently Asked Questions (FAQ) about Private Medical Insurance

Is private medical insurance worth it?

The value of private medical insurance is subjective. It offers benefits like faster access and greater choice, which can be invaluable for many. For others, the public health system might suffice. It often comes down to personal priorities regarding convenience, speed, and financial comfort.

Can I cancel my private medical insurance anytime?

Most policies allow you to cancel, but specific terms will apply. You might be liable for a portion of the premium for the period you were covered. Always check your policy’s terms and conditions regarding cancellation.

Is private medical insurance tax-deductible?

In many regions, private medical insurance premiums are not tax-deductible for individuals, though there can be exceptions for specific scenarios or for businesses providing it to employees. It’s important to consult with a tax advisor or review local tax laws.

What if I travel abroad with private medical insurance?

Standard private medical insurance typically covers treatment within your home country. For travel abroad, you would generally need separate travel insurance that includes medical coverage. Some premium policies might offer limited international coverage, but this is not the norm.

Conclusion

Private medical insurance can be a powerful tool for safeguarding your health and providing peace of mind. By understanding the different types of plans, the factors influencing costs, and how to navigate common clauses like pre-existing conditions, you can make an informed choice that aligns with your individual needs and budget. It’s an investment in your health, offering flexibility and control over your medical care.

Your Health, Your Choice: Take the Next Step

Ready to explore your options for private medical insurance? We encourage you to research reputable providers, compare quotes, and carefully review policy details. For further reading on financial planning and insurance, consider resources like Investopedia. Don’t hesitate to consult with a qualified independent financial advisor or insurance broker to get personalized advice tailored to your unique circumstances. Taking control of your health decisions starts with education and careful planning.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.