Navigating student loan debt can feel overwhelming, but for many dedicated individuals, a powerful program offers a path to freedom: the Public Service Loan Forgiveness (PSLF) program. This guide will walk you through everything you need to know about this vital opportunity, from understanding eligibility to submitting your final application. If you’ve committed your career to serving the public, unlocking public service loan forgiveness could dramatically reduce or even eliminate your federal student loan debt.

Simply put, the Public Service Loan Forgiveness (PSLF) program is designed to forgive the remaining balance on your federal direct loans after you’ve made 120 qualifying monthly payments while working full-time for an eligible employer. It’s a huge benefit for nurses, teachers, government employees, and many others. This isn’t just about debt relief; it’s about recognizing the invaluable contributions of public servants.

Who Qualifies for Public Service Loan Forgiveness?

Understanding eligibility is the first critical step for PSLF. There are three core requirements: your loans, your employer, and your payment history. You must have eligible federal direct loans, work full-time for a qualifying employer, and make 120 qualifying payments.

Why this matters in real life: Many people assume their job qualifies without checking, leading to years of payments that won’t count. It’s essential to verify your employer’s eligibility early on.

Eligible Employment: Your Service Counts

To qualify, you must work for a U.S. federal, state, local, or tribal government organization, including the military. Non-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code also qualify. This includes most charities, hospitals, and educational institutions.

- Government Organizations: This includes federal agencies, state governments, public schools, public hospitals, and even local city halls.

- 501(c)(3) Non-Profits: Think of organizations like the American Red Cross, Habitat for Humanity, or your local food bank.

- Other Non-Profits: Certain other non-profit organizations that provide specific public services (like public health or education) may qualify, even if they aren’t 501(c)(3) organizations. Check with StudentAid.gov for specifics.

Scenario: Imagine you are a social worker earning $45,000 to $60,000 annually at a non-profit serving underprivileged youth. As long as your employer is a 501(c)(3) organization and you work at least 30 hours per week, your employment likely qualifies. If you instead worked for a for-profit counseling service, even one helping similar clients, your employment would not qualify for PSLF.

Eligible Loans: Direct Loans Only

Only loans under the William D. Ford Federal Direct Loan Program are eligible for PSLF. This includes Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, and Direct Consolidation Loans.

Why this matters in real life: Many older federal loans, like Federal Family Education Loans (FFEL) or Perkins Loans, do not qualify directly. You must consolidate them into a Direct Consolidation Loan to become eligible. This consolidation must happen before you make payments you want to count towards PSLF.

The 120 Qualifying Payments Explained

The core of PSLF is making 120 qualifying monthly payments. This doesn’t mean you just make payments for 10 years; specific conditions must be met for each payment to count.

Why this matters in real life: Missing even one condition can invalidate payments, delaying your forgiveness or making you ineligible. Tracking your payments is crucial.

- Made on Time: Payments must be made no later than 15 days after your due date.

- Full Amount: Each payment must be for the full amount due as shown on your bill.

- Under a Qualifying Repayment Plan: This is critical. You must be on an Income-Driven Repayment (IDR) plan. Standard 10-year plans only qualify if your payment equals what you’d pay on an IDR plan, which is rarely the case for those seeking forgiveness.

- While Employed: You must be working full-time for a qualifying employer when you make the payment.

Example: Sarah is a public school teacher with $70,000 in Direct Loans. She enrolls in an IDR plan, which calculates her monthly payment based on her income. For 10 years (120 months), she consistently makes her payments on time while working full-time. During a brief period of unemployment, she skips a payment. That specific payment will not count towards her 120, but she can resume counting once she is re-employed and making qualifying payments.

Income-Driven Repayment (IDR) Plans: Your PSLF Partner

Income-Driven Repayment (IDR) plans are the linchpin of PSLF. These plans adjust your monthly payment based on your income and family size, making payments more affordable, especially for those in public service careers that may not always offer high salaries.

Why this matters in real life: If you’re not on an IDR plan, your payments generally won’t count towards PSLF. This is where many applicants make a critical error, thinking any payment plan works.

There are several IDR plans, including:

- Saving on a Valuable Education (SAVE) Plan: This is the newest IDR plan, offering potentially lower payments and expanded interest benefits.

- Pay As You Earn (PAYE) Repayment Plan

- Income-Based Repayment (IBR) Plan

- Income-Contingent Repayment (ICR) Plan

Each plan has slightly different calculations for monthly payments. It’s crucial to explore which one best fits your financial situation, as lower payments under IDR plans mean more debt remains to be forgiven by PSLF.

Mini Case Study: David is a government paralegal earning $55,000 annually with $80,000 in student loan debt. On a Standard 10-year plan, his monthly payment might be around $800. On a SAVE plan, his payment could be reduced to $300-$400 depending on his family size. By paying $350 monthly instead of $800, he saves thousands over 10 years and ensures his payments count towards public service loan forgiveness.

Step-by-Step Guide to PSLF

Successfully navigating PSLF requires proactive steps. Follow this guide to stay on track.

- Confirm Loan Eligibility: Ensure you have Direct Loans. If not, consolidate other federal loans into a Direct Consolidation Loan. Visit StudentAid.gov to review your loan types.

- Enroll in an Income-Driven Repayment (IDR) Plan: Apply for an IDR plan through your loan servicer or directly on StudentAid.gov. Reapply annually to keep your payments adjusted to your income.

- Verify Employer Eligibility: Use the PSLF Help Tool on StudentAid.gov to confirm your employer qualifies. This tool also helps generate the Employment Certification Form (ECF).

- Submit the Employment Certification Form (ECF) Annually: Submit this form to your loan servicer regularly (at least once a year, or whenever you change jobs). This allows your servicer to track your qualifying payments and confirm your employer’s eligibility. This is arguably the most critical step to avoid future headaches.

- Track Your Progress: Your loan servicer will notify you of your qualifying payment count after processing your ECF. Monitor this closely for any discrepancies.

- Apply for Forgiveness: After making 120 qualifying payments, submit the PSLF Application to your loan servicer. They will review your entire history for final approval.

How to Calculate Your Potential Savings

Understanding the financial impact of PSLF can be incredibly motivating. While we can’t provide exact figures, here’s a practical way to think about your potential savings.

First, determine your likely monthly payment under an Income-Driven Repayment (IDR) plan. This is usually a percentage (e.g., 10%) of your discretionary income, which is your income minus a certain percentage of the federal poverty line. For example, if your discretionary income is $30,000, and your IDR plan charges 10%, your payment would be $300 per month.

Multiply this monthly payment by 120 (for 10 years). This is your total out-of-pocket cost. Then, subtract this from your original loan balance. The remaining amount is what could be forgiven.

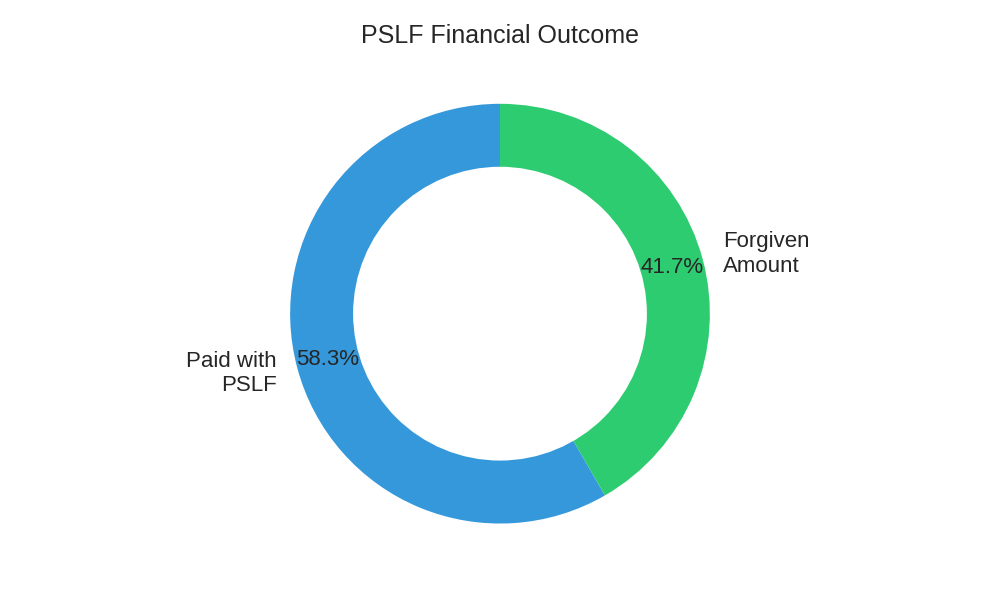

Example: Let’s say you have an initial loan balance of $60,000 at a 6% interest rate. Your standard 10-year payment might be around $666 per month, totaling $79,920 paid over 10 years. However, if your income-driven payment is only $300 per month due to your public service salary, you would pay $300 x 120 = $36,000 over 10 years. The remaining balance (potentially over $24,000, plus accrued interest) would be forgiven.

The actual amount forgiven can be substantial. The benefit increases with higher loan balances and lower income-driven payments.

PSLF Forgiveness Estimator

| Loan Details | Standard 10-Year Repayment (No PSLF) | Income-Driven Repayment (with PSLF) |

|---|---|---|

| Initial Loan Balance | $75,000 | $75,000 |

| Approx. Monthly Payment (Range) | $800 – $850 | $350 – $450 (Income-driven) |

| Total Paid Over 10 Years | $96,000 – $102,000 | $42,000 – $54,000 |

| Potential Forgiven Amount | $0 | $30,000 – $40,000+ |

Note: These are illustrative ranges. Actual amounts depend on specific interest rates, income, and family size.

Common Pitfalls and How to Avoid Them

Many applicants encounter issues that delay or prevent their forgiveness. Being aware of these common mistakes can save you significant time and stress.

- Not Consolidating FFEL/Perkins Loans: Many older federal loans don’t qualify directly. Consolidate them into a Direct Consolidation Loan early. Don’t wait until you’ve made years of payments.

- Incorrect Repayment Plan: The biggest pitfall is not being on an IDR plan. Payments made on a Standard 10-year, Extended, or Graduated plan typically won’t count.

- Not Submitting ECF Annually (or When Changing Jobs): Failing to submit the Employment Certification Form regularly means your servicer isn’t tracking your payments. You could make years of payments and not have them counted.

- For-Profit Employer: Working for a for-profit organization, even one performing public-like services, will not qualify. Always verify eligibility.

- Not Working Full-Time: PSLF requires full-time employment (at least 30 hours per week). If you work part-time for multiple qualifying employers, the combined hours can sometimes count.

Scenario: Consider Maria, a nurse who worked for eight years at a private, for-profit hospital, making payments on an IDR plan. She then moved to a county public hospital. Only her payments made while at the public hospital will count towards PSLF. Her prior eight years of payments, despite being on an IDR plan, will not qualify because her employer was not eligible.

For more detailed guidance and to understand all requirements, always refer to official sources like the Consumer Financial Protection Bureau (CFPB) or U.S. Department of Education.

Frequently Asked Questions (FAQ)

Q1: Is PSLF taxable income?

No. Under current law, the amount of your loan forgiven through PSLF is not considered taxable income by the IRS. This is a significant advantage compared to some other forms of loan forgiveness.

Q2: What if I change jobs? Do my payments still count?

If you change jobs, your past qualifying payments still count towards your 120 total. However, your new employer must also be a qualifying public service employer. You should submit a new Employment Certification Form (ECF) with your new employer as soon as possible.

Q3: Do I have to make 120 consecutive payments?

No, the 120 payments do not need to be consecutive. You could work for a qualifying employer, leave public service for a few years, and then return. Payments made during the break would not count, but you can pick up where you left off once you resume qualifying employment and payments.

Q4: What happens if my loan servicer changes?

If your loan servicer changes, your payment history and PSLF progress should automatically transfer to the new servicer. Continue to submit your ECFs to your new servicer and keep detailed records of all your payments and communications.

Q5: Can I get credit for past payments I made before knowing about PSLF?

Under certain circumstances, and particularly during limited waiver periods, past payments that didn’t originally qualify might be counted. Always check StudentAid.gov for the latest information on temporary changes or waivers, as rules can evolve.

Conclusion

The Public Service Loan Forgiveness program offers an incredible opportunity for public servants to achieve financial freedom. While it requires diligence and careful tracking, the reward of erasing federal student loan debt is well worth the effort. By understanding the eligibility criteria, choosing the right repayment plan, and consistently submitting your Employment Certification Forms, you can successfully navigate the path to forgiveness.

Your Call to Action: Take Control of Your Debt

Don’t let complexity deter you. Start today by visiting StudentAid.gov. Use the PSLF Help Tool to verify your employer, check your loan types, and get on track for public service loan forgiveness. Your service is invaluable – let this program help you thrive financially.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.