Want to lower your monthly mortgage payments, pay off your home faster, or access your home equity? A mortgage refinance could be your most powerful financial tool. This comprehensive guide will demystify the mortgage refinance process, helping you save thousands and achieve your financial goals. Understanding when and how to execute a successful mortgage refinance is key to unlocking significant savings over the life of your loan.

In essence, refinancing means replacing your current mortgage with a new one. This new loan typically comes with different terms, such as a lower interest rate, a shorter loan period, or the option to take cash out. It’s a strategic move to improve your financial standing, but it requires careful consideration of current market conditions and your personal circumstances.

Why Consider a Mortgage Refinance?

There are several compelling reasons homeowners choose to refinance their mortgage, each offering distinct financial advantages. Understanding these benefits is the first step in deciding if a mortgage refinance is right for you.

Lower Your Interest Rate and Monthly Payments

This is perhaps the most common reason. If interest rates have dropped since you originally financed your home, you could secure a lower rate. Why does this matter in real life? Even a small reduction, say from 4.5% to 3.5%, can translate into significant savings on your monthly payment and over the entire life of the loan. Imagine you currently pay $1,500 per month on your mortgage. A refinance could reduce that to $1,300, freeing up an extra $200 in your budget every single month.

Shorten Your Loan Term

If you’ve been in your home for a few years and your financial situation has improved, you might be able to refinance from a 30-year loan to a 15-year loan. This will likely increase your monthly payment, but it drastically reduces the total interest you’ll pay and gets you mortgage-free much sooner. For example, moving from a 30-year to a 15-year mortgage could shave hundreds of thousands of dollars off your total interest paid, allowing you to build equity faster.

Tap into Home Equity with a Cash-Out Refinance

A cash-out refinance allows you to borrow more than you owe on your current mortgage and receive the difference in cash. This can be a smart way to finance major expenses, like home renovations, college tuition, or debt consolidation, often at a lower interest rate than personal loans or credit cards. For instance, if your home is worth $400,000, and you owe $200,000, you might be able to borrow up to $320,000 (80% loan-to-value), receiving $120,000 in cash. It’s crucial to use this responsibly, as you are increasing your mortgage debt.

Switch Loan Types

You might want to switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage for stability, especially if interest rates are rising. Conversely, some might move from fixed to ARM if rates are expected to fall, though this carries more risk. Why this matters? A fixed-rate mortgage offers predictable payments, protecting you from future rate hikes and making budgeting easier.

Understanding the Mortgage Refinance Process

Refinancing involves several steps, similar to your original home purchase. Knowing what to expect can make the journey smoother.

- Assess Your Goals: Before anything else, define why you want to refinance. Is it to lower your payment, shorten your term, or get cash out? Your goal will dictate the type of refinance best suited for you. Why this matters? Clear goals help you choose the right product and avoid unnecessary costs.

- Check Your Credit Score: Lenders look for strong credit. A score of 720 or higher typically qualifies you for the best rates. If your score is lower, consider improving it before applying to get more favorable terms. Why this matters? A better credit score can save you thousands in interest over the life of the loan.

- Gather Documents: Prepare financial documents like pay stubs, W-2s, tax returns, bank statements, and current mortgage statements. Having these ready streamlines the application process.

- Shop Around for Lenders: Don’t just go with your current lender. Get quotes from at least three to five different lenders to compare interest rates, fees, and closing costs. This competitive shopping is vital. The Consumer Financial Protection Bureau (CFPB) offers resources to help you understand mortgage options and shop effectively. You can learn more at consumerfinance.gov.

- Submit Your Application: Once you choose a lender, complete the formal application. They will pull your credit report and verify your income and assets.

- Underwriting and Appraisal: The lender’s underwriting department will review your entire financial profile. An appraisal will be ordered to determine your home’s current market value, and title insurance will be required. Why this matters? The appraisal ensures the loan amount doesn’t exceed a safe percentage of your home’s value.

- Closing: After approval, you’ll attend a closing meeting to sign all the final loan documents. You will pay closing costs at this stage, which typically range from 2% to 5% of the loan amount.

- Rescission Period: For most refinances on a primary residence, there’s a three-day “right of rescission” period, allowing you to cancel the loan without penalty. The new loan will fund after this period.

How to Calculate Your Potential Savings

Calculating whether a refinance makes financial sense involves more than just looking at the new interest rate. You need to factor in all costs and long-term implications.

Start by comparing your current interest rate and monthly payment to what you expect with a new loan. Multiply your new estimated monthly payment by the new loan term (for instance, 360 months for a 30-year loan) to find your new total estimated cost. Subtract this from your old total estimated cost. Remember to account for all closing costs associated with the new loan.

For example, if your current mortgage balance is around $250,000 at a 4.5% interest rate, and you can refinance to 3.5%, your monthly payment will decrease. However, if closing costs are $5,000, you need to determine how long it will take for your monthly savings to offset that $5,000. This is known as your break-even point.

To calculate your break-even point:

- Determine your total closing costs for the refinance.

- Calculate the difference in your monthly payment (current minus new).

- Divide the total closing costs by your monthly savings. The result is the number of months it will take to recoup your refinance costs.

Why this matters in real life? If you plan to sell your home before reaching your break-even point, a refinance might not save you money and could even cost you more. You can also explore various calculators online to help estimate these figures, such as those provided by financial institutions or independent sites like Bankrate.com.

Refinance Your Mortgage Save Thousands Now

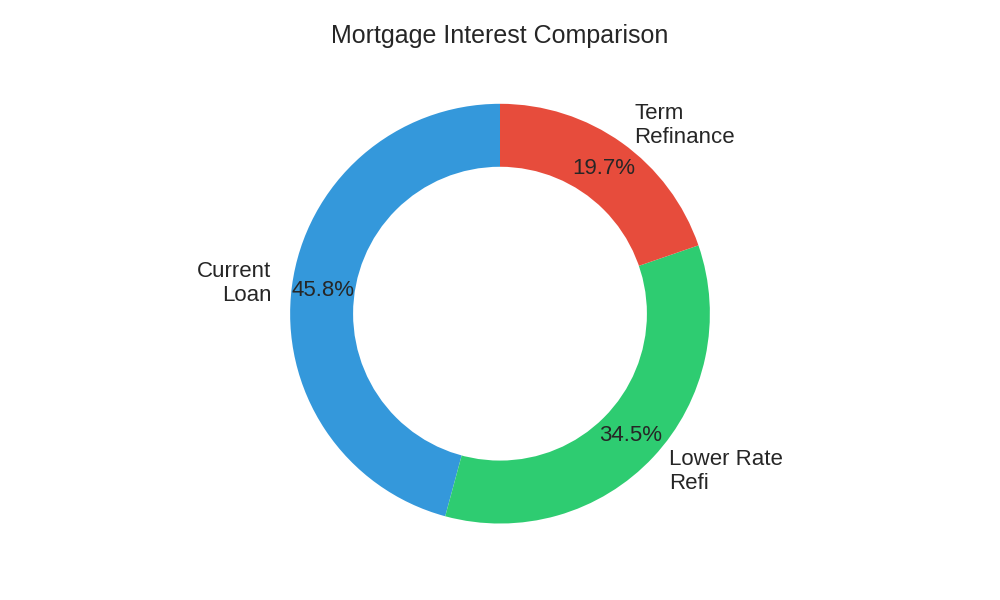

Understanding the full financial picture is crucial. Here’s a comparative table illustrating potential long-term impacts:

| Scenario | Loan Balance (Approx.) | Interest Rate | Original Term Remaining | Estimated New Monthly Payment | Total Interest Paid (Est.) | Est. Lifetime Savings (vs. Original) |

|---|---|---|---|---|---|---|

| Current Mortgage | $300,000 | 4.50% | 25 years | $1,667 | ~$199,999 | N/A |

| Refinance Option 1 (Lower Rate) | $300,000 | 3.50% | 25 years | $1,502 | ~$150,578 | ~$49,421 |

| Refinance Option 2 (Shorter Term) | $300,000 | 3.50% | 15 years | $2,145 | ~$86,131 | ~$113,868 |

Note: These are illustrative examples. Actual savings depend on specific loan terms, closing costs, and individual financial situations.

Common Refinance Costs to Expect

Just like your original mortgage, a refinance comes with costs, often called closing costs. These are fees paid to the lender and various third parties involved in the transaction. Why does this matter? If closing costs are too high, they can eat into your savings, potentially making the refinance less beneficial in the short term.

- Origination Fees: What the lender charges for processing the loan.

- Appraisal Fee: Cost for a professional to assess your home’s value.

- Title Insurance: Protects the lender (and sometimes you) against claims of ownership on your property.

- Recording Fees: Paid to your local government to record the new mortgage.

- Escrow Fees: Charges for the neutral third party handling the transaction.

- Prepaid Interest and Property Taxes: Funds collected to cover interest from closing to the first payment, and potentially property taxes.

Closing costs typically range from 2% to 5% of the loan amount. You can often roll these costs into your new mortgage, but this means you’ll pay interest on them over the life of the loan. Alternatively, you can pay them upfront at closing to reduce your principal.

When is the Best Time to Refinance?

The ideal time for a refinance is highly personal, but a few key indicators can signal a good opportunity. Generally, if interest rates have fallen by at least 0.75% to 1.00% since you took out your current mortgage, it’s worth investigating. Also, consider your credit score: if it has significantly improved, you may qualify for much better rates. Finally, if you’ve been in your home long enough to build substantial equity, a cash-out refinance might be an option for major financial projects. You can monitor current mortgage rates through resources like the Federal Reserve, which provides economic data and trends relevant to interest rates on their website: federalreserve.gov.

FAQ: Addressing Common Doubts About Mortgage Refinancing

Many homeowners have questions when considering a refinance. Here are some answers to common concerns:

Q: How often can I refinance my mortgage?

A: There’s no strict limit, but each refinance incurs closing costs. It only makes sense if the savings outweigh these costs. Most people refinance every 5-10 years, or when rates significantly drop.

Q: Will refinancing restart my loan term?

A: Not necessarily. You can choose a new loan term (e.g., 15, 20, or 30 years) that aligns with your goals. If you’ve paid on your current 30-year mortgage for five years, you could refinance into a new 25-year mortgage to keep a similar payoff timeline, or a 15-year for a faster payoff.

Q: What if my home value has decreased?

A: A decrease in home value can make refinancing harder, as lenders prefer a certain loan-to-value (LTV) ratio. If your LTV is too high (meaning you owe almost as much as your home is worth), you might not qualify for conventional refinancing. Government programs like the FHA Streamline Refinance or VA Interest Rate Reduction Refinance Loan (IRRRL) might be options if you have those types of loans, often requiring less equity.

Q: Do I need a perfect credit score to refinance?

A: While a higher credit score (typically 720+) gets you the best rates, you don’t need to be perfect. Many lenders offer programs for scores in the mid-600s, though your interest rate might be higher. Improving your score before applying can lead to better terms.

Q: Should I use a mortgage broker or go directly to a lender?

A: Both have pros and cons. Brokers work with multiple lenders to find you the best deal, potentially saving you time. Direct lenders might offer specific in-house products or promotions. It’s wise to explore both options to ensure you’re getting competitive offers.

Conclusion

A mortgage refinance can be a powerful financial decision, offering opportunities to reduce monthly payments, save on interest, or access home equity. However, it’s not a one-size-fits-all solution. Careful consideration of your financial goals, current market conditions, and the associated costs is essential. By understanding the process and thoroughly shopping for the best terms, you can leverage a refinance to significantly improve your financial health.

Ready to explore your options? Start by reviewing your current mortgage statement and researching today’s interest rates. Talk to several lenders to get personalized quotes and assess whether a refinance aligns with your long-term financial strategy. Taking action today could lead to substantial savings tomorrow!

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.