You’ve poured your heart and soul into building your business. You know the potential, you see the growth opportunities, but you also feel the pinch – the need for capital to take that next big step. Applying for an SBA loan can feel like navigating a maze, a path fraught with regulations, paperwork, and often, frustrating denials. Many ambitious entrepreneurs share your experience, encountering unexpected obstacles on their journey to secure crucial funding. This article isn’t about the basic application steps; it’s about dissecting the toughest hurdles and providing actionable solutions. We’re here to help you master the challenges of obtaining an SBA loan, transforming potential setbacks into stepping stones for your business’s future.

Understanding the Common Roadblocks to SBA Loan Approval

When you seek an SBA loan, it’s easy to feel overwhelmed by the application process. You might encounter specific pain points that can derail your efforts. Let’s look at the most common reasons why promising businesses face setbacks, so you can proactively address them.

Credit Score Concerns

Your personal and business credit scores are often the first gatekeepers to any significant financing. Lenders use these scores to assess your reliability in managing debt. A low score doesn’t necessarily mean you’re irresponsible, but it signals a higher risk to lenders. You might have had past financial challenges, or perhaps you’re a relatively new business without much established credit history. This can be a major stumbling block when trying to secure an SBA loan.

Insufficient Collateral or Guarantees

While SBA loans are known for lower collateral requirements compared to conventional loans, you might still face challenges. Lenders want assurance that if your business defaults, there’s a way to recover some of their investment. You might find yourself struggling to present enough tangible assets, or personal guarantees might feel like too big a risk. This often leaves you in a bind, unable to meet the lender’s security expectations.

An Unclear or Weak Business Plan

Your business plan is more than just a document; it’s your story, your vision, and your financial roadmap. Lenders need to see a clear, compelling narrative that demonstrates viability and growth potential. If your plan lacks detail, projections are unrealistic, or your market analysis is weak, it can raise serious red flags. You might know your business inside and out, but failing to articulate it effectively on paper can severely hamper your application for an SBA loan.

High Debt-to-Income (DTI) or Debt Service Coverage Ratio (DSCR)

Lenders meticulously scrutinize your existing debt and your ability to comfortably take on more. If your personal DTI is too high, or your business’s DSCR suggests you barely cover your current debt obligations, adding a new loan becomes a significant risk. You might feel trapped by existing financial commitments, making it hard to prove you have the capacity to manage new ones. This financial tightrope walk is a common pain point for many entrepreneurs.

Crafting Your Winning Application: Solutions and Strategies

Facing these hurdles can be daunting, but they are not insurmountable. You have the power to transform these pain points into areas of strength. By proactively addressing these common issues, you significantly increase your chances of securing the funding your business needs to thrive.

Bolstering Your Credit Profile

Improving your credit score takes time and discipline, but it’s a worthwhile investment. Start by checking your personal and business credit reports for errors and disputing them immediately. Focus on paying bills on time, reducing existing debt, and keeping credit utilization low. Consider strategies like becoming an authorized user on a well-managed credit card to build history, or securing a small business credit card to establish a separate business credit file. For a comprehensive guide on building business credit, you can refer to resources like NerdWallet’s guide to building business credit.

Maximizing Collateral Opportunities

Don’t underestimate the value of all your assets. Beyond real estate, consider inventory, accounts receivable, or equipment as potential collateral. If personal guarantees are required, ensure you fully understand the implications and communicate transparently with your lender. Sometimes, a strong business case and a solid repayment history can outweigh a slight collateral deficit. Explore all avenues and discuss flexible options with your prospective lenders.

Developing a Robust Business Plan

Your business plan needs to be a living document, not just a one-off for the loan application. Ensure it includes a compelling executive summary, detailed market analysis, clear marketing and sales strategies, a strong management team description, and most importantly, realistic and well-supported financial projections. Demonstrate your understanding of your industry and your unique competitive advantage. Seek feedback from mentors or business advisors to refine your plan before submission. The SBA itself offers excellent resources and templates for business planning, which you can find on their official website: SBA.gov Business Guide.

Managing Your Financial Ratios

Before applying, meticulously review your financial statements. Work to reduce unnecessary expenses, improve cash flow, and pay down existing high-interest debt. Aim for a strong debt service coverage ratio (DSCR) – ideally 1.25:1 or higher for many lenders. This means your net operating income is at least 1.25 times your total debt payments. Be prepared to explain any fluctuations or historical challenges in your financial performance, always emphasizing your path to improvement.

The Importance of a Strong Lender Relationship

Choosing the right lender is as crucial as perfecting your application. Seek out banks that specialize in SBA loans and have a strong track record of approvals. Develop a rapport with their lending officers. They can provide invaluable guidance, point out potential weaknesses in your application before submission, and even offer alternative solutions. A good relationship can make all the difference in navigating the complexities of the SBA loan process.

Understanding Your Loan Repayment: A Practical Example

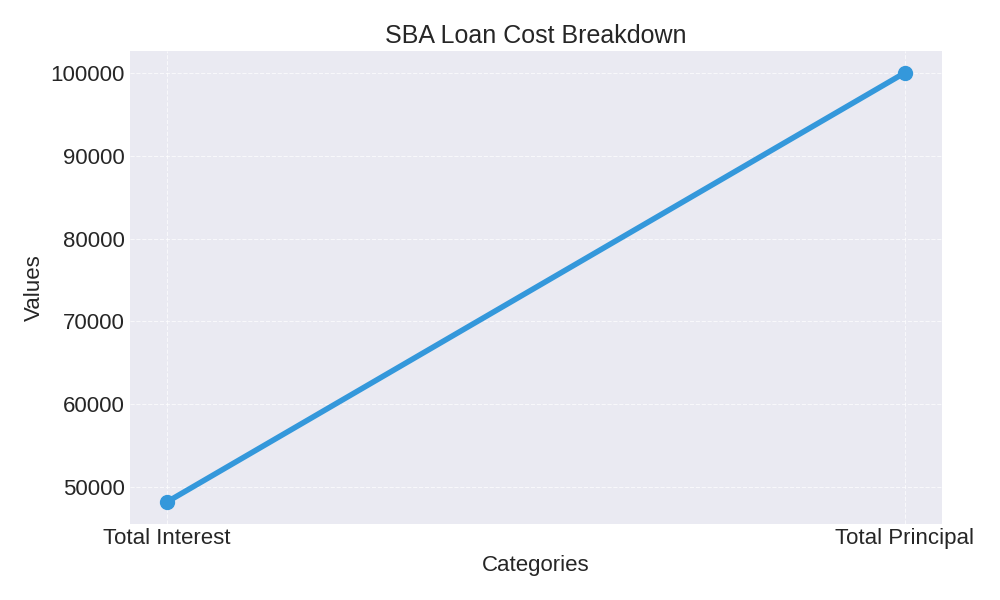

Securing an SBA loan is just the first step; understanding its repayment is critical for your financial health. You need to know exactly what your monthly obligations will be and how much interest you’ll pay over the life of the loan. Let’s look at a simplified example to illustrate this. If you borrow $100,000 at an 8.5% annual interest rate over a 10-year term, your monthly payment will remain consistent, but the proportion of principal and interest in each payment will change over time. Initially, more of your payment goes towards interest, gradually shifting to more principal as the loan matures. This predictable structure helps you budget effectively.

| Year | Remaining Balance | Monthly Payment |

|---|---|---|

| 1 | $93,519.00 | $1,245.59 |

| 3 | $77,090.00 | $1,245.59 |

| 5 | $57,010.00 | $1,245.59 |

| 7 | $32,670.00 | $1,245.59 |

| 10 | $0.00 | $1,245.59 |

In this scenario, over 10 years, you would pay a total of approximately $149,471, which includes the $100,000 principal and roughly $49,471 in total interest. Understanding these numbers upfront helps you make informed decisions and budget accurately for your business’s future financial obligations. Tools like an amortization calculator can provide precise breakdowns for different scenarios. For more detailed insights into loan amortization and its calculations, you might find Investopedia’s explanation of amortization helpful.

Monthly Payment Calculator

Beyond the Basics: Advanced Strategies for Success

Sometimes, simply ticking the boxes isn’t enough. You might need to explore additional avenues and leverage expert insights to truly stand out.

Leveraging Professional Guidance

Don’t try to go it alone. Business consultants, accountants, and SBA-preferred lenders often have deep expertise in navigating the application process. They can help you identify weaknesses, optimize your financial statements, and present your case most effectively. An experienced professional can be a game-changer, helping you to refine your strategy and avoid common pitfalls. The upfront investment in professional advice can save you significant time and potentially secure the funding you need.

Understanding Different SBA Programs

The SBA offers various loan programs, each designed for specific business needs. The 7(a) loan is the most common, but you might also consider SBA 504 loans for real estate or equipment, or even microloans for smaller amounts. Researching the nuances of each program allows you to choose the one that best aligns with your business goals and financial situation. Don’t assume one size fits all; finding the right program can make the difference between approval and denial. Familiarize yourself with all the options available directly from the source by visiting the SBA website and reviewing the most up-to-date eligibility requirements and terms. Consulting with an SBA-approved lender can also provide valuable insight into which program fits your profile. Proper preparation and program selection increase your chances of securing favorable financing. A well-matched SBA loan can support sustainable growth and long-term business success.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.