Life is unpredictable. One moment you’re healthy and productive, the next an unexpected illness or injury could prevent you from working. How would you cover your bills if your paycheck suddenly stopped? This is precisely where short term disability insurance steps in, acting as a crucial safety net for your income.

In essence, short term disability insurance provides a portion of your income when you’re unable to work for a temporary period due to a non-work-related injury, illness, or even pregnancy. It’s a vital financial tool that prevents a health crisis from becoming a financial catastrophe, ensuring you don’t lose your paycheck when you need it most.

Understanding Short Term Disability Insurance: Your Income Shield

Short term disability insurance is a type of coverage designed to replace a percentage of your income if you become temporarily disabled and cannot perform your job duties. This disability could stem from various causes, such as a broken leg, a serious illness, or complications during pregnancy and childbirth.

Why does this matter in real life? Imagine you’re a single parent earning a steady income, and suddenly you need surgery that requires a 10-week recovery period. Without short term disability insurance, your income would cease, making it impossible to pay rent, groceries, and other essential bills. This insurance bridges that financial gap, providing peace of mind during a challenging time.

How Short Term Disability Insurance Works

Navigating the specifics of short term disability insurance involves understanding a few key terms and processes. These typically include waiting periods, benefit periods, and the percentage of income replacement.

- Waiting Period (Elimination Period): This is the time between when your disability starts and when your benefits begin. It’s often around 7 to 14 days for illnesses, though it might be shorter for injuries. For instance, if you break your arm and your policy has a 7-day waiting period, you won’t receive benefits for the first week you’re out of work. This period reduces the insurer’s risk and your premium.

- Benefit Period: This is the maximum length of time you can receive benefits. For short term disability, it typically ranges from 3 to 6 months, but can extend up to a year. Once this period ends, if you’re still unable to work, a long term disability policy would usually take over, if you have one.

- Benefit Amount: Policies typically replace 40% to 70% of your gross income, with 60% being a common figure. This percentage helps ensure you have sufficient funds to cover essential expenses without fully replacing your salary, which also helps prevent fraud.

Who Needs Short Term Disability Insurance?

While some employers offer this benefit, many individuals and small businesses do not have it. Almost anyone who relies on their income to cover living expenses can benefit from this coverage. It’s particularly crucial for those who:

- Have limited emergency savings (less than 3-6 months’ worth of expenses).

- Do not have employer-provided disability benefits.

- Are self-employed and would lose all income if unable to work.

- Have dependents who rely on their income.

Consider a scenario where Sarah, a freelance graphic designer, breaks her ankle and can’t use her computer for six weeks. As an independent contractor, she has no paid sick leave. If she has an individual short term disability policy, she can receive a portion of her income during her recovery, preventing her business and personal finances from collapsing.

Calculating Your Potential Benefits

Understanding how much you might receive from a short term disability policy is straightforward once you know the key figures. You don’t need complex formulas, just basic multiplication. Here’s a practical approach:

First, find your gross monthly income. This is your income before taxes and other deductions. For example, if you earn an annual salary of $60,000, your gross monthly income is $5,000.

Next, identify your policy’s income replacement percentage. This is usually provided as a specific percentage, such as 60%.

To estimate your monthly benefit, simply multiply your gross monthly income by the income replacement percentage. So, using our example: $5,000 (gross monthly income) multiplied by 0.60 (60%) equals $3,000.

This means you would receive approximately $3,000 per month in benefits, before any tax implications or deductions applied by the insurer or employer. Remember, this is an estimate, and actual benefits may vary based on policy specifics and tax laws.

Short Term Disability Insurance Don't Lose Your Paycheck

Factors Influencing Premiums and Policy Details

The cost and specific terms of your short term disability insurance policy can vary widely. Several factors play a role in determining your premiums:

- Your Age: Younger individuals typically pay less because they are generally less likely to experience a disability.

- Your Health and Medical History: Pre-existing conditions or a history of certain health issues can lead to higher premiums or exclusions.

- Your Occupation: High-risk jobs (e.g., construction workers) typically have higher premiums than lower-risk office jobs.

- Income to be Replaced: The higher the percentage of income you want to replace, the higher your premium will be.

- Waiting Period Length: A longer waiting period (e.g., 30 days instead of 7 days) usually results in lower premiums.

- Benefit Period Length: A shorter benefit period (e.g., 3 months instead of 6 months) often means lower premiums.

For example, a healthy 30-year-old in an office job might pay between $20-$50 per month for a policy, while a 50-year-old with a physically demanding job might pay significantly more, perhaps $70-$150 per month for similar coverage. It’s always wise to compare quotes.

| Scenario Detail | Without STD Insurance (6-month disability) | With STD Insurance (60% income replacement) |

|---|---|---|

| Monthly Gross Income (Example) | $4,500 | $4,500 |

| Lost Income per Month | $4,500 | $1,800 (40% of gross) |

| STD Benefit per Month | $0 | $2,700 (60% of gross) |

| Total Income Received During Disability (6 months) | $0 | $16,200 |

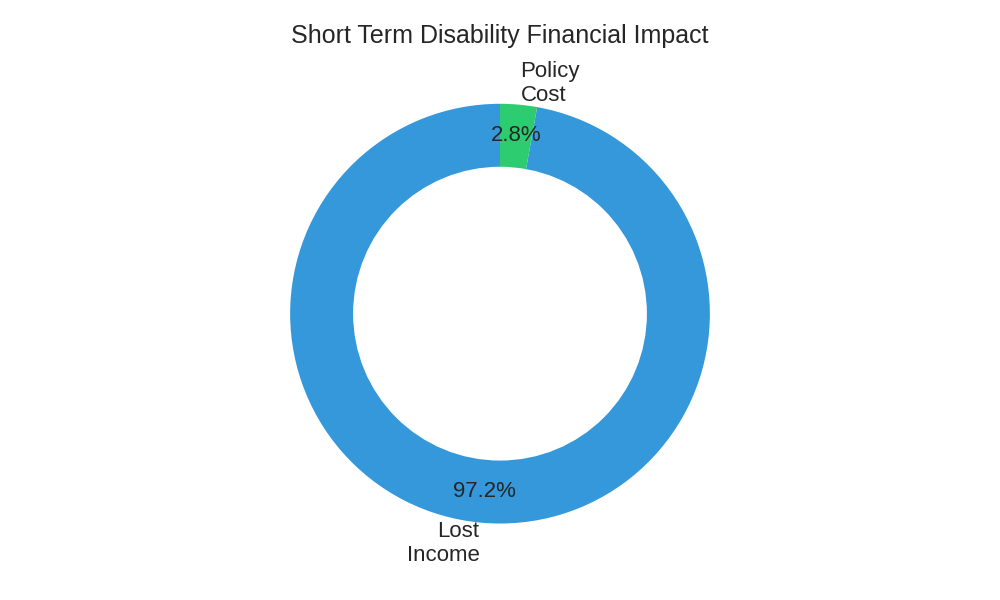

| Total Lost Income Over 6 Months | $27,000 | $10,800 |

| Estimated Monthly Policy Cost | N/A | $30-$75 |

| Total Policy Cost (6 months) | N/A | $180-$450 |

| Net Financial Impact (approx.) | -$27,000 | -$11,250 (Lost Income + Policy Cost) |

This table illustrates the significant financial protection offered by short term disability insurance, turning a potential total income loss into a manageable reduction.

Frequently Asked Questions About Short Term Disability

Q1: Is short term disability insurance taxable?

A: It depends. If your employer pays the premiums, the benefits you receive are generally taxable. If you pay the premiums with after-tax dollars, the benefits are typically tax-free. Always consult a tax professional for specific advice regarding your situation. You can find more general information on taxation of benefits from the Internal Revenue Service.

Q2: Can I get short term disability if I have a pre-existing condition?

A: It’s possible, but there might be limitations. Most policies have a “look-back period” (e.g., 3-12 months) during which conditions treated or diagnosed may not be covered for a certain period after the policy takes effect. It’s crucial to disclose all medical history when applying and understand the policy’s specific clauses.

Q3: What’s the difference between short term and long term disability insurance?

A: The main difference is the duration of the benefit period. Short term disability covers a temporary inability to work, typically for a few months up to a year. Long term disability kicks in after short term benefits expire and can provide income replacement for many years, sometimes until retirement age. Think of short term as immediate relief and long term as sustained support for severe, extended disabilities.

Q4: Do all employers offer short term disability?

A: No. While some states mandate temporary disability insurance (TDI) programs, it is not a federal requirement. Many employers offer it as a voluntary benefit, while others do not. You can check if your state has a TDI program by visiting your state’s Department of Labor website, such as the U.S. Department of Labor site for an overview of labor laws.

Q5: Is pregnancy covered by short term disability?

A: Yes, in most cases, normal pregnancy and childbirth are considered a short term disability, covering the time you are medically unable to work, including recovery time. This typically falls under employer-sponsored or individual policies. The specific duration of covered leave varies by policy and state laws.

Conclusion: Protect Your Financial Future

Short term disability insurance is an often-overlooked yet critical component of a robust personal financial plan. It provides an essential safety net, ensuring that an unexpected illness or injury doesn’t derail your financial stability. Without it, a temporary health setback could lead to significant debt, jeopardizing your home, savings, and overall well-being. Don’t assume you’re covered or that it won’t happen to you.

Take Action Now: Review your current benefits with your employer, explore individual policy options, and understand the terms. Proactive planning today can provide invaluable peace of mind tomorrow. Protect your paycheck and secure your financial future.

For more insights into managing financial risks, consider exploring resources from reputable financial education organizations like the Consumer Financial Protection Bureau.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.