Unlock the secrets to significant wealth growth by mastering your investing returns. Many believe strong returns are reserved for the financial elite, but with the right knowledge and strategy, anyone can enhance their investment performance. This guide will demystify complex financial concepts, making them accessible and actionable, so you can confidently navigate the path to smarter investing.

At its core, maximizing your investing returns involves understanding how your money grows, actively managing risks, and leveraging the power of time and consistency. By the end of this comprehensive guide, you’ll possess the tools and insights to both calculate and strategically improve your investment outcomes, moving you closer to your financial goals.

Understanding Investing Returns: The Core Concepts

Before you can optimize your investment performance, you must first grasp what “returns” truly represent. It’s more than just the money you get back; it’s about the growth your capital experiences over a specific period.

What Are Investing Returns?

In simple terms, an investing return is the gain or loss on an investment over a specified period, expressed as a percentage of the initial investment. It reflects how much profit (or loss) you’ve made relative to the money you put in. Positive returns mean your investment has grown, while negative returns indicate a loss.

Types of Returns

When we talk about investing returns, several types come into play:

- Capital Gains: This is the profit you make when you sell an asset (like stocks or real estate) for a higher price than you paid for it. For instance, buying a stock at $50 and selling it at $70 yields a capital gain of $20 per share.

- Income Returns: These are recurring payments generated by your investments. Examples include dividends from stocks, interest from bonds or savings accounts, and rental income from properties.

- Total Return: This is the most comprehensive measure, combining both capital gains and income returns. It gives you the full picture of your investment’s performance.

Risk vs. Return: A Fundamental Relationship

A crucial concept in investing is the relationship between risk and return. Generally, investments with the potential for higher returns also carry higher risk, meaning a greater chance of losing your initial capital. Conversely, lower-risk investments tend to offer more modest returns. Understanding your risk tolerance is paramount to choosing suitable investments that align with your financial objectives.

How to Calculate Your Investing Returns (Without Complex Math)

Calculating your investment returns might sound daunting, but it can be broken down into straightforward steps. You don’t need advanced formulas to get a clear picture of your progress.

Simple Return Calculation

To calculate a basic, or “absolute,” return, you simply compare your investment’s ending value to its starting value. This is useful for understanding the overall gain or loss.

Here’s how to do it:

- Find your Ending Value: This is how much your investment is worth now.

- Find your Starting Value: This is how much you initially invested.

- Calculate the Change: Subtract the Starting Value from the Ending Value.

- Divide by the Starting Value: Take the change and divide it by your original investment.

- Multiply by 100: This converts your result into a percentage.

Example: You invested $1,000, and it’s now worth $1,200.

Change = $1,200 – $1,000 = $200

Return = ($200 / $1,000) * 100 = 20%

Annualized Return (for investments held longer than a year)

To compare investments held for different durations, you’ll want to calculate an annualized return, which shows your average annual gain. For simplicity, if your total return is X% over Y years, and growth was relatively steady, you can approximate by dividing X by Y for a rough annual average. However, for precise comparisons, especially with fluctuating values, financial tools or advisors are recommended. Many online brokers provide these calculations automatically.

Remember, these calculations give you a snapshot. Always consider the impact of fees, taxes, and inflation, which can erode your real returns over time. Understanding how to calculate your investing returns is the first step towards taking control of your financial future.

Strategies to Maximize Your Investing Returns

Achieving superior investing returns isn’t about finding a single “secret stock” but rather implementing a combination of proven strategies consistently over time.

1. Diversification: Don’t Put All Your Eggs…

Diversification involves spreading your investments across various asset classes (stocks, bonds, real estate), industries, and geographic regions. This strategy helps reduce risk because if one investment performs poorly, others may perform well, balancing your overall portfolio. This prudent approach is strongly advocated by regulatory bodies like the U.S. Securities and Exchange Commission (SEC).

2. Compounding: The Eighth Wonder of the World

Compound interest is interest earned on both the initial principal and the accumulated interest from previous periods. Reinvesting your earnings allows your money to grow exponentially over time. The earlier you start investing, the more powerful compounding becomes, turning modest initial investments into substantial wealth.

3. Long-Term Horizon: Patience Pays Off

Investing with a long-term perspective allows your investments to weather market fluctuations and capitalize on the upward trend of the market over decades. Short-term trading can be highly speculative and risky, whereas a long-term strategy often yields more consistent and significant returns.

4. Reinvesting Dividends: Fueling Growth

If you own dividend-paying stocks or funds, choosing to reinvest those dividends to buy more shares is a powerful way to accelerate compounding. This simple action can significantly boost your total returns over many years without requiring additional cash contributions from you.

5. Cost Control: Fees Eat Away at Returns

High fees, whether from management expenses, trading commissions, or mutual fund expense ratios, can significantly erode your investing returns. Always be mindful of the costs associated with your investments and choose low-cost options whenever possible. Every percentage point saved in fees is a percentage point added to your actual return.

6. Regular Contributions: Dollar-Cost Averaging

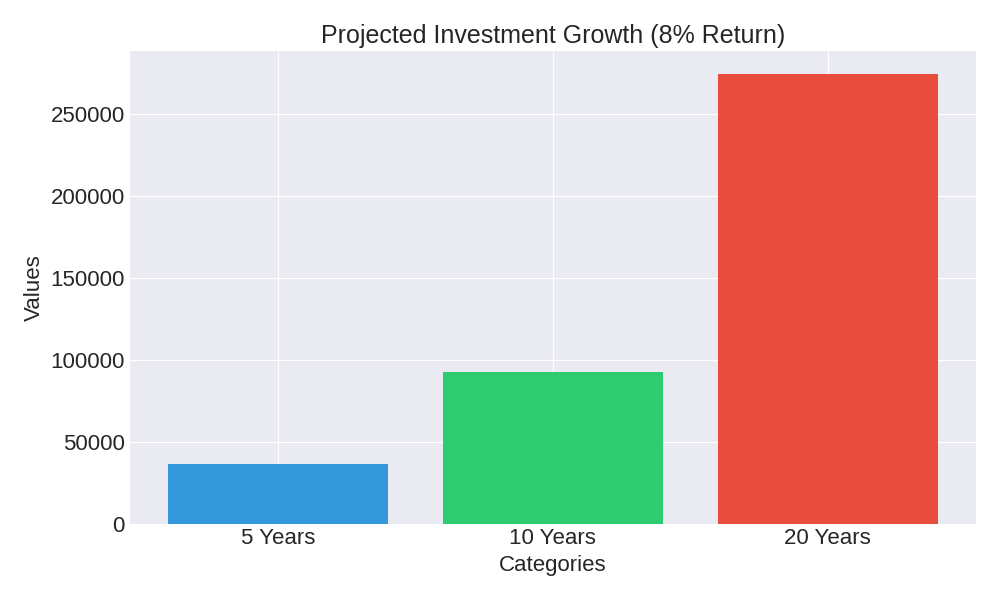

Dollar-cost averaging involves investing a fixed amount of money at regular intervals, regardless of market conditions. This strategy helps mitigate risk by averaging out your purchase price over time. When prices are high, you buy fewer shares; when they are low, you buy more. This disciplined approach often leads to better long-term results than trying to “time the market.”

| Investment Horizon | Total Contribution | Projected Value (8% Annual Return) |

|---|---|---|

| Year 5 | $30,000 ($500/month) | $36,602 |

| Year 10 | $60,000 ($500/month) | $92,618 |

| Year 20 | $120,000 ($500/month) | $274,519 |

*This table illustrates the power of compounding with regular contributions. Assumes a consistent $500 monthly investment at an 8% annual return. Actual returns may vary.

Common Pitfalls to Avoid

Even with the best strategies, certain mistakes can severely undermine your investing returns.

- Emotional Decisions: Reacting impulsively to market ups and downs, like panic selling during a downturn or chasing “hot” stocks, often leads to poor outcomes. Stick to your long-term plan.

- Lack of Research: Investing in something you don’t understand is akin to gambling. Always do your due diligence or consult with a qualified professional. Resources from organizations like FINRA can help you research effectively.

- Ignoring Inflation: Inflation erodes the purchasing power of your money over time. While your nominal returns might look good, your real return (after inflation) could be much lower. Always aim for returns that outpace inflation.

Frequently Asked Questions (FAQ)

Q: What’s a “good” investing return?

A: What constitutes a “good” return depends heavily on your investment’s risk level, time horizon, and economic conditions. Historically, the stock market has averaged around 7-10% annually over long periods, but past performance is not indicative of future results. For conservative investments like bonds, returns are typically lower. The most important thing is that your returns help you achieve your personal financial goals.

Q: How does inflation affect my returns?

A: Inflation reduces the purchasing power of your money. If your investment earns 5% but inflation is 3%, your “real” return is only 2%. It’s crucial for your investments to generate returns that significantly exceed the rate of inflation to grow your wealth effectively. Economic factors, which are often influenced by policies from institutions like the Federal Reserve, play a large role in inflation.

Q: Should I worry about taxes on my returns?

A: Absolutely. Taxes can significantly impact your net investing returns. Capital gains, dividends, and interest are generally taxable. Understanding tax-advantaged accounts (like 401(k)s and IRAs) and tax-efficient investing strategies can help minimize your tax burden and maximize your take-home returns. Always consult a tax professional for personalized advice.

Conclusion

Mastering the art of smart investing returns is a journey, not a destination. It requires continuous learning, discipline, and a commitment to proven strategies. By understanding the core concepts of returns, knowing how to calculate them, and applying strategies like diversification, compounding, and cost control, you empower yourself to make informed decisions that can lead to substantial wealth accumulation over time.

Take Control of Your Financial Future

Don’t let the complexity of finance deter you. Start small, stay consistent, and continually educate yourself. The power to achieve your financial dreams lies in smart, strategic investing. Begin today by reviewing your current investments, setting clear goals, and applying the principles outlined in this guide. If you’re unsure, consider consulting a qualified financial advisor to help tailor a plan specific to your unique situation and objectives.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.