Navigating the complex world of student loan debt can feel overwhelming, a burden that lingers long after graduation. For many, the dream of a debt-free future seems distant, overshadowed by monthly payments and accruing interest. However, understanding the various pathways to student loan forgiveness can transform this daunting challenge into a manageable journey. This comprehensive guide will illuminate the options available, helping you identify opportunities to significantly reduce or even eliminate your student debt. We’ll break down the requirements and processes, empowering you to take control of your financial future.

Understanding Student Loan Forgiveness Programs

Student loan forgiveness refers to programs that cancel a portion or all of a borrower’s federal student loan debt. These programs are typically designed to support individuals in specific professions, those experiencing financial hardship, or those whose schools engaged in misconduct. It’s crucial to understand that federal student loan forgiveness is distinct from deferment or forbearance, which only temporarily pause payments.

Eligibility for these programs varies significantly based on factors such as your loan type, employment, income, and enrollment history. Identifying the correct program for your situation is the first step toward potential relief. Private student loans, unfortunately, are generally not eligible for federal forgiveness programs.

Types of Federal Student Loan Forgiveness Programs

The U.S. Department of Education offers several programs designed to provide relief from federal student loan debt. Each program has unique requirements and benefits.

Public Service Loan Forgiveness (PSLF)

The Public Service Loan Forgiveness (PSLF) program is designed to forgive the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments under a qualifying repayment plan while working full-time for a qualifying employer. This typically includes government organizations (federal, state, local, or tribal) and not-for-profit organizations.

- Eligibility: You must have Direct Loans, work full-time for a qualifying employer, be on an income-driven repayment (IDR) plan, and make 120 qualifying payments.

- Benefit: The entire remaining balance of your Direct Loans is forgiven, tax-free.

- Official Source: For detailed information and to confirm employer eligibility, visit the official Federal Student Aid PSLF page.

Income-Driven Repayment (IDR) Plan Forgiveness

Income-Driven Repayment (IDR) plans make your monthly student loan payments more affordable by basing them on your income and family size. After a certain period of payments (typically 20 or 25 years, depending on the plan and whether you have graduate or undergraduate loans), any remaining balance on your federal student loans is forgiven.

- Types of IDR Plans: The most common plans include the SAVE Plan (Saving on a Valuable Education), PAYE (Pay As You Earn), IBR (Income-Based Repayment), and ICR (Income-Contingent Repayment).

- Eligibility: Most federal student loans are eligible. You must apply annually to re-certify your income and family size.

- Benefit: Remaining loan balance forgiven after 20-25 years of payments. Note that this forgiven amount may be subject to federal income tax, though temporary exemptions have been in place.

Teacher Loan Forgiveness

This program is for teachers who teach full-time for five complete and consecutive academic years in certain low-income schools or educational service agencies. You may be eligible for up to $17,500 in forgiveness for Direct Subsidized and Unsubsidized Loans and Federal Stafford Loans.

- Eligibility: Highly qualified teacher, five consecutive years in a low-income school, specific loan types.

- Benefit: Up to $17,500 in forgiveness, depending on the subject taught (e.g., highly qualified math or science teachers at the secondary level, or special education teachers).

Perkins Loan Cancellation

Federal Perkins Loans were awarded to students with exceptional financial need, though the program ended in 2017. If you have outstanding Perkins Loans, you may qualify for cancellation based on your employment in certain public service occupations, such as teaching, nursing, law enforcement, or early childhood development. The percentage of the loan cancelled increases over time.

- Eligibility: Specific public service professions and a qualifying Perkins Loan.

- Benefit: Partial or full loan cancellation over a period of years.

Total and Permanent Disability (TPD) Discharge

If you have a total and permanent disability, you may be eligible to have your federal student loans discharged. This means you will no longer be required to repay them.

- Eligibility: You must meet specific criteria for a total and permanent disability, typically verified by the Department of Veterans Affairs, Social Security Administration, or a physician.

- Benefit: Complete discharge of eligible federal student loans.

Borrower Defense to Repayment

This program offers loan forgiveness if your school misled you or engaged in other misconduct in violation of certain state laws. This could include misrepresenting job placement rates, program costs, or the quality of education.

- Eligibility: Evidence that your school committed fraud or other misconduct related to your federal student loans.

- Benefit: Full or partial discharge of your federal student loans.

Closed School Discharge

If your school closes while you’re enrolled, or soon after you withdraw, you might be eligible for a full discharge of your federal student loans. This applies if you were unable to complete your program due to the closure.

- Eligibility: Your school closed, and you meet specific enrollment or withdrawal criteria without completing your program or transferring credits to a similar program.

- Benefit: Full discharge of eligible federal student loans.

Eligibility and Application Process

Applying for student loan forgiveness requires careful attention to detail and understanding your specific situation. The process can vary significantly depending on the program.

Step-by-Step Guide to Applying for Forgiveness

- Understand Your Loan Types: First, determine if your loans are federal or private. Only federal loans qualify for most forgiveness programs. You can check your federal loan status on StudentAid.gov.

- Research Eligible Programs: Based on your employment, income, and educational history, identify which forgiveness programs you might qualify for.

- Consolidate if Necessary: Some programs, like PSLF, require Direct Loans. If you have FFEL Program loans or Perkins Loans, you may need to consolidate them into a Direct Consolidation Loan.

- Enroll in an IDR Plan: For PSLF and IDR forgiveness, you must be enrolled in an eligible income-driven repayment plan.

- Track Payments and Employment: Keep meticulous records of all payments made and employment verification forms, especially for PSLF. Use the PSLF Help Tool on StudentAid.gov.

- Submit the Application: Complete the specific application form for your chosen program. This often involves submitting documentation to your loan servicer or the Department of Education.

The Math of Repayment and Forgiveness

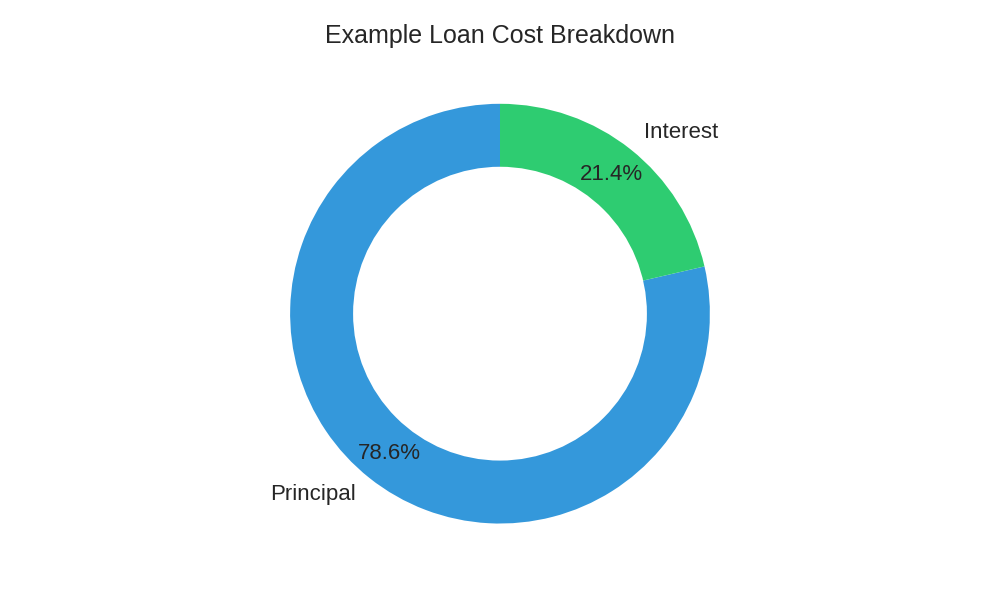

Understanding how interest accrues and how payments reduce your principal is crucial, even when pursuing forgiveness. While the specifics can get complex, the basic principle is straightforward: borrowed principal plus accumulated interest determines your total repayment amount. Forgiveness programs aim to reduce or eliminate this burden.

For example, if you borrow $30,000 at 5% interest over a standard 10-year repayment plan, your monthly payment would be around $318. Your total repayment over the life of the loan would be approximately $38,160, meaning you pay over $8,000 in interest alone. Forgiveness programs aim to cut down on this total cost or even eliminate the outstanding principal.

| Year | Remaining Balance | Monthly Payment (Estimate) |

|---|---|---|

| 1 | $27,800 | $318 |

| 5 | $16,500 | $318 |

| 10 | $0 | $318 |

Monthly Payment Calculator

Understanding how your payments are distributed between principal and interest is key. Early payments often cover more interest, while later payments tackle more principal. Programs like PSLF or IDR forgiveness essentially step in to cover the remaining principal and interest after you meet specific service or payment criteria, potentially saving you tens of thousands of dollars. It’s also important to consider the tax implications of forgiven debt; while PSLF is tax-free, IDR forgiveness traditionally has been taxable income, though this has seen temporary changes. Financial experts at Bloomberg often discuss such policy nuances.

Common Pitfalls and How to Avoid Them

While student loan forgiveness offers significant relief, many borrowers encounter obstacles. Being aware of these common pitfalls can help you navigate the process more smoothly.

- Not Tracking Payments Diligently: For programs like PSLF, every qualifying payment counts. Keep detailed records and submit your PSLF Employment Certification Form regularly.

- Ignoring Loan Type Restrictions: Private student loans are almost never eligible for federal forgiveness programs. Confirm your loan types on StudentAid.gov.

- Misunderstanding Program Requirements: Each program has specific criteria (e.g., full-time employment, specific loan types, income levels). Carefully review all requirements to ensure you qualify before committing to a plan.

- Failing to Re-certify Annually for IDR: If you are on an Income-Driven Repayment plan, you must re-certify your income and family size each year. Failing to do so can lead to increased payments and capitalized interest.

- Scam Alert: Be wary of companies promising “guaranteed” loan forgiveness for a fee. Official forgiveness programs are free to apply for, and you should always work directly with your loan servicer or StudentAid.gov.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.