Navigating the world of student financing can feel like a complex maze, especially when you encounter terms like student loan private loans. For many aspiring students, understanding the nuances between federal and private funding is crucial for making informed decisions about their education and future financial health. This comprehensive guide will demystify private student loans, helping you understand what they are, how they work, and what you need to consider before taking them on.

Simply put, private student loans are educational loans offered by private lenders like banks, credit unions, and state-affiliated organizations, rather than the federal government. Unlike federal loans, they often come with variable interest rates, fewer borrower protections, and depend heavily on your creditworthiness. This guide will provide you with the essential knowledge to approach student loan private loans with confidence, ensuring you make choices that align with your long-term financial goals.

Understanding Student Loan Private Loans vs. Federal Loans

The primary distinction between federal and private student loans lies in their origin and the benefits they offer. Federal student loans are issued by the U.S. Department of Education, providing a range of protections like income-driven repayment plans, forbearance, deferment options, and potential forgiveness programs. They don’t typically require a credit check for most undergraduates.

Student loan private loans, on the other hand, originate from private financial institutions. Their terms, interest rates, and repayment options vary significantly by lender. Lenders typically conduct a credit check and often require a co-signer, especially for students with limited credit history. Why does this matter in real life? The type of loan you choose dictates your flexibility and safety net if you face financial hardship after graduation.

Imagine you are comparing two loan offers. One is a federal Stafford loan, and the other is a private loan from a bank. The federal loan might have a slightly higher interest rate initially but offers an income-driven repayment plan that adjusts your monthly payments if your post-graduation salary is lower than expected. The private loan might offer a tempting low variable interest rate, but if you lose your job, your monthly payments won’t change, potentially leading to default. This scenario highlights the importance of understanding the long-term implications of each loan type beyond just the interest rate.

Here’s a quick comparison of key differences:

- Lender: Federal Government vs. Banks, Credit Unions, etc.

- Interest Rates: Fixed and often lower for federal vs. Fixed or variable, often higher for private.

- Credit Check: Not typically required for federal (undergrad) vs. Always required for private.

- Borrower Protections: Extensive (IDR, deferment, forbearance, forgiveness) vs. Limited to none.

- Loan Limits: Set limits for federal vs. Often higher, based on cost of attendance for private.

When Student Loan Private Loans Make Sense

While federal loans are generally the first and best option, there are specific situations where student loan private loans can be a necessary or even strategic choice. These usually arise when federal aid limits are exhausted, or for specific academic programs.

For example, if you’re pursuing a specialized graduate degree that requires significant funding beyond federal loan limits—perhaps a medical or law degree—private loans might be essential to cover the remaining costs. Similarly, if your parents’ income disqualifies you from substantial need-based federal aid, but they are unable to contribute significantly to your education, private loans could bridge the gap.

Eligibility Requirements and Application Process

Unlike federal loans, eligibility for private loans hinges largely on your creditworthiness. Lenders will examine your credit score, income, and debt-to-income ratio. Since most students have a limited credit history, a co-signer is often required.

A co-signer is someone (usually a parent or guardian) with good credit who agrees to share legal responsibility for the loan. Imagine your credit score is 620, which is typically considered “fair.” A private lender might deny your application or offer a very high interest rate. However, if your parent with a 780 “excellent” score co-signs, the lender sees reduced risk and might offer a much more favorable rate. This co-signer impact can save you thousands of dollars over the life of the loan. It matters because a good co-signer can be the difference between getting an affordable loan and being denied or stuck with exorbitant rates.

Navigating Interest Rates and Repayment Options

One of the most critical aspects of student loan private loans is understanding their interest rates and repayment structures. Private loans typically offer either fixed interest rates or variable interest rates.

A fixed rate remains the same throughout the life of the loan, providing predictable monthly payments. A variable rate can change periodically (e.g., quarterly or annually) based on market indexes, meaning your payments can go up or down. While variable rates might start lower, they introduce risk. If interest rates rise, your payments could become significantly higher than anticipated. This matters in real life because it directly impacts your budget and financial stability over the long term.

Repayment options for private loans are generally less flexible than federal loans. Most private lenders offer immediate repayment, deferred repayment (payments start after graduation), or interest-only repayment during school. Always read the fine print to understand what options are available if you face unforeseen financial challenges. For comprehensive information on protecting yourself from deceptive practices, consult resources like the Consumer Financial Protection Bureau at consumerfinance.gov.

How to Calculate Your Potential Loan Cost

Estimating the total cost of your private student loan involves understanding the loan amount, interest rate, and repayment term. While lenders provide repayment calculators, here’s a simple way to think about it without complex formulas. The goal is to see how much extra you’ll pay beyond the initial borrowed amount.

Let’s say you borrow $10,000. If your interest rate is, for example, 5% and you pay it back over 10 years, you’ll make 120 payments. Each payment covers a portion of the principal (the original $10,000) and the interest that has accrued. In the beginning, a larger part of your payment goes towards interest. As you pay down the loan, more of your payment goes towards the principal.

To get a rough idea: take your total loan amount. Multiply it by your annual interest rate. This gives you a ballpark of the interest you’d pay in one year on the full amount. For a 10-year loan, you’re looking at that amount multiplied by 10, plus some complexity for compounding and principal reduction. The key takeaway is that higher interest rates and longer repayment periods significantly increase the total amount you repay.

PRIVATE STUDENT LOAN PAYMENT & COST ESTIMATOR

Monthly Payment: $0.00

Total Amount Paid: $0.00

Total Interest Paid: $0.00

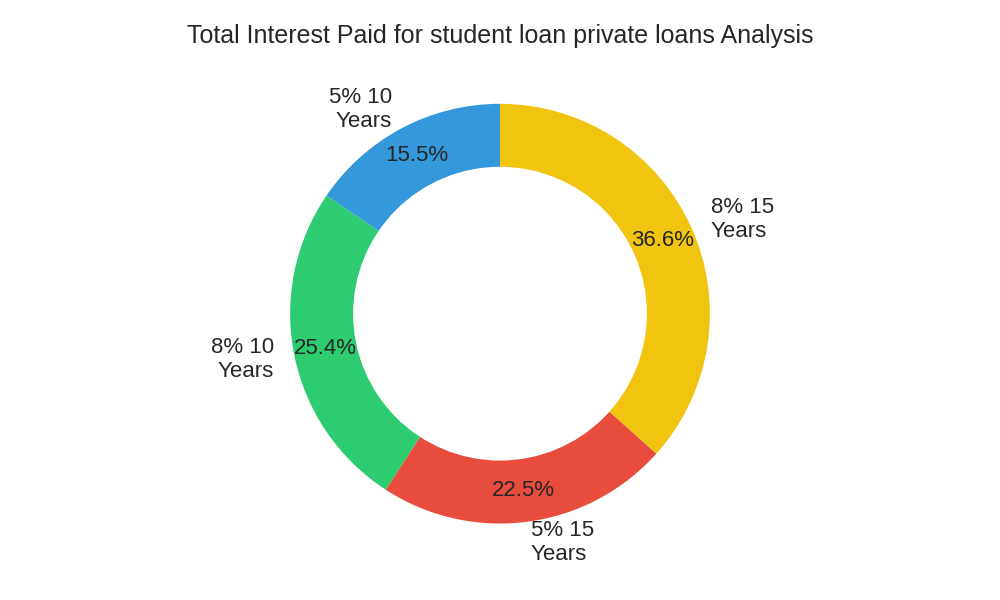

Here’s a simple scenario illustrating how different interest rates and terms can affect the total cost of a $20,000 private loan:

| Loan Amount | Interest Rate | Repayment Term | Estimated Total Interest Paid | Estimated Total Payback |

|---|---|---|---|---|

| $20,000 | 5% (Fixed) | 10 Years | ~$5,500 – $6,000 | ~$25,500 – $26,000 |

| $20,000 | 8% (Fixed) | 10 Years | ~$9,000 – $9,500 | ~$29,000 – $29,500 |

| $20,000 | 5% (Fixed) | 15 Years | ~$8,000 – $8,500 | ~$28,000 – $28,500 |

| $20,000 | 8% (Fixed) | 15 Years | ~$13,000 – $14,000 | ~$33,000 – $34,000 |

Potential Risks and Drawbacks of Private Student Loans

While private loans can be a lifeline, it’s crucial to acknowledge their significant drawbacks. The biggest risk lies in the lack of borrower protections compared to federal loans. Federal loans offer a robust safety net, including income-driven repayment (IDR) plans that adjust your monthly payment based on your income and family size. They also provide options for deferment or forbearance during periods of unemployment or economic hardship, and even pathways to loan forgiveness for public service workers.

In a typical scenario, imagine you graduate and struggle to find a job in your field, or perhaps you experience a sudden medical emergency. If you have federal loans, you could apply for forbearance, temporarily pausing your payments, or enroll in an IDR plan to significantly lower them. With private loans, your lender might offer limited forbearance options, or none at all. This means your monthly payments remain high, potentially leading to missed payments, damaged credit, or even default. Understanding these risks is vital for informed borrowing.

Smart Strategies for Managing Student Loan Private Loans

Even if you’ve taken out private loans, there are proactive steps you can take to manage them effectively and minimize their long-term cost.

- Exhaust Federal Options First: Always fill out the Free Application for Federal Student Aid (FAFSA) to maximize eligibility for grants, scholarships, and federal loans before considering private options. You can find comprehensive information on federal student aid at studentaid.gov.

- Shop Around for Lenders: Don’t just accept the first offer. Compare interest rates, fees, and repayment terms from multiple private lenders to find the most favorable deal.

- Consider a Co-signer: If your credit isn’t strong, a co-signer can help you secure a lower interest rate. Ensure your co-signer understands their responsibilities.

- Refinance When Possible: If you’ve improved your credit score or income since taking out the loan, consider refinancing your student loan private loans. Refinancing involves taking out a new loan with a lower interest rate to pay off your old loans. This can significantly reduce your total interest paid and lower your monthly payments. For example, if you took out a private loan at 8% and after a few years your credit score improved and market rates dropped, you might qualify to refinance at 5%, saving you thousands over the remaining loan term.

- Make Extra Payments: If your budget allows, making extra payments—even small ones—can reduce your principal faster and save on interest. Aim to pay more than the minimum required whenever you can.

- Automate Payments: Many lenders offer a small interest rate discount (e.g., 0.25%) for setting up automatic payments. This also ensures you never miss a payment.

Frequently Asked Questions (FAQ)

Can private student loans be forgiven?

Generally, no. Unlike federal student loans, private student loans typically do not offer loan forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment forgiveness. There are very limited circumstances, like death or permanent disability, where the loan might be discharged, but these are rare and depend on the specific lender’s policy. For more insights on loan types and their implications, Investopedia offers valuable resources at investopedia.com.

Do private student loans impact my credit score?

Yes, significantly. When you apply for a private loan, lenders perform a hard inquiry on your credit report, which can temporarily lower your score. Successfully making on-time payments will build positive credit history, while missed or late payments will negatively impact your score. This is why managing private loans responsibly is crucial for your financial future.

Is it possible to consolidate private student loans?

Yes, it is possible. You can consolidate multiple private student loans (and often federal loans, though it means losing federal protections) by refinancing them into a single new private loan. This typically results in one monthly payment and can potentially secure a lower overall interest rate if your credit has improved since you first borrowed.

What happens if I can’t pay my private student loans?

If you struggle to make payments, immediately contact your lender. Some lenders may offer limited forbearance or deferment options, but these are not guaranteed. Failure to pay can lead to late fees, a damaged credit score, collection efforts, and potentially legal action. Unlike federal loans, private lenders have fewer options for flexible repayment plans if you’re experiencing hardship.

Conclusion

Understanding student loan private loans is a critical step in financing your education responsibly. While they lack the comprehensive protections of federal loans, they can be a necessary tool when federal aid is insufficient. By carefully evaluating interest rates, repayment terms, and potential risks, and by implementing smart management strategies like refinancing, you can navigate private student loans effectively.

Always prioritize federal aid first, but if private loans are part of your financial plan, approach them with diligence and a clear understanding of your obligations. Your financial future depends on these choices. Take the time to research thoroughly and consider speaking with a financial advisor to ensure your borrowing strategy aligns with your long-term goals.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.