Navigating the world of higher education often means confronting the complex reality of a student loan. For many aspiring students, securing funding is an essential step towards achieving their academic and career goals. However, the path to obtaining a student loan can be fraught with potential pitfalls, leading to significant debt if not approached with careful planning and understanding. This comprehensive guide will walk you through the fundamentals, helping you make informed decisions and manage your educational debt effectively. Understanding the various types of loans, their terms, and repayment strategies is crucial to avoid the burden of crushing debt after graduation.

Understanding Student Loans: Federal vs. Private

A student loan is money borrowed to finance education, typically covering tuition, fees, room and board, books, and living expenses. These loans must be repaid, usually with interest, after the student leaves school or drops below half-time enrollment. Understanding the distinction between federal and private loans is the first critical step.

Federal Student Loans

Federal loans are funded by the U.S. government and offer numerous benefits and protections not typically found with private options. They are generally considered the best starting point for most students.

- Fixed Interest Rates: Federal loans often come with fixed interest rates, meaning your rate won’t change over the life of the loan, providing predictability in your payments.

- Income-Driven Repayment (IDR) Plans: These plans adjust your monthly payments based on your income and family size, making repayment more manageable during periods of lower earnings.

- Deferment and Forbearance: Options to temporarily postpone payments are available under specific circumstances, such as economic hardship or military service.

- Loan Forgiveness Programs: Certain federal loans may be eligible for public service loan forgiveness (PSLF) or teacher loan forgiveness programs.

- No Credit Check (for most undergraduate loans): Unlike private loans, many federal loans do not require a credit check, making them accessible to younger students without established credit.

There are different types of federal loans, including Subsidized Direct Loans (government pays interest while in school), Unsubsidized Direct Loans (interest accrues immediately), PLUS Loans for parents and graduate students, and Consolidation Loans. For more details on federal student aid programs, visit the official student aid website: studentaid.gov.

Private Student Loans

Private loans are offered by banks, credit unions, and other financial institutions. They are often used to bridge the gap between the cost of attendance and the amount covered by federal aid, scholarships, and savings.

- Variable Interest Rates: Many private loans have variable interest rates, which can fluctuate with market conditions, potentially leading to higher payments over time.

- Credit-Based Approval: Private lenders typically require a strong credit history and income, often necessitating a co-signer for students.

- Fewer Repayment Protections: Private loans generally offer fewer flexible repayment options, deferment, or forbearance programs compared to federal loans.

- No Loan Forgiveness: Private loans are not eligible for federal loan forgiveness programs.

It’s generally recommended to exhaust all federal loan options, grants, and scholarships before considering private loans due to their often less favorable terms.

The Application Process: Steps to Securing Funding

The application process for student loans differs significantly between federal and private options. Understanding these steps is crucial for timely and successful funding.

Step-by-Step Federal Loan Application

The gateway to federal student aid is the Free Application for Federal Student Aid (FAFSA).

- Complete the FAFSA: Fill out the FAFSA form annually. This form determines your eligibility for federal student aid, including grants, work-study, and federal loans.

- Receive Your Student Aid Report (SAR): After submitting the FAFSA, you’ll receive a SAR summarizing your eligibility. Review it carefully for accuracy.

- Review Financial Aid Offers: Each school you’re accepted to will send you a financial aid offer package. Compare these offers, noting the mix of grants, scholarships, and federal loans.

- Accept and Sign: Accept the aid you need and complete any necessary loan entrance counseling and sign a Master Promissory Note (MPN).

The FAFSA opens on October 1st each year, and it’s essential to submit it as early as possible to meet state and institutional deadlines, as some aid is awarded on a first-come, first-served basis.

Step-by-Step Private Loan Application

Applying for private loans involves a different set of considerations, primarily focusing on creditworthiness.

- Determine Your Need: Calculate how much funding you still require after exhausting federal aid and other resources.

- Research Lenders: Compare multiple private lenders, looking at interest rates, repayment terms, fees, and borrower benefits. Websites like NerdWallet or Bankrate can be good starting points for comparison.

- Check Your Credit Score: If you have a credit history, review it for accuracy. If you don’t, be prepared to apply with a co-signer.

- Complete the Application: Provide personal, financial, and academic information as requested by the lender.

- Review Loan Disclosure: Carefully read the loan agreement, understanding all terms, conditions, and repayment obligations before signing.

A co-signer can significantly improve your chances of approval and potentially secure a lower interest rate for a private student loan.

Interest Rates and How They Work

Understanding interest is paramount for any borrower. Interest is essentially the cost of borrowing money, calculated as a percentage of the principal (the original amount borrowed).

Understanding Interest Accrual

For federal loans, interest often doesn’t start accruing until after you leave school, especially for subsidized loans. For unsubsidized federal loans and private loans, interest typically begins to accrue immediately. This means interest is added to your principal balance from day one, even while you’re still in school. This phenomenon is known as capitalization when unpaid interest is added to the principal balance, increasing the total amount on which future interest is calculated.

Fixed vs. Variable Interest Rates

- Fixed Interest Rates: Your interest rate remains the same throughout the entire life of the loan. This provides stability and predictability for your monthly payments. Federal student loans exclusively offer fixed rates.

- Variable Interest Rates: Your interest rate can change over time, typically tied to a market index like the prime rate or LIBOR. This means your monthly payments could increase or decrease, making budgeting more challenging. Private student loans often feature variable rates.

How to Calculate Your Student Loan Payments

While the exact mathematical formulas for loan amortization can be complex, the principle is straightforward: your monthly payment covers both a portion of the principal and the accrued interest. Over time, as you pay down the loan, more of your payment goes towards the principal, and less towards interest.

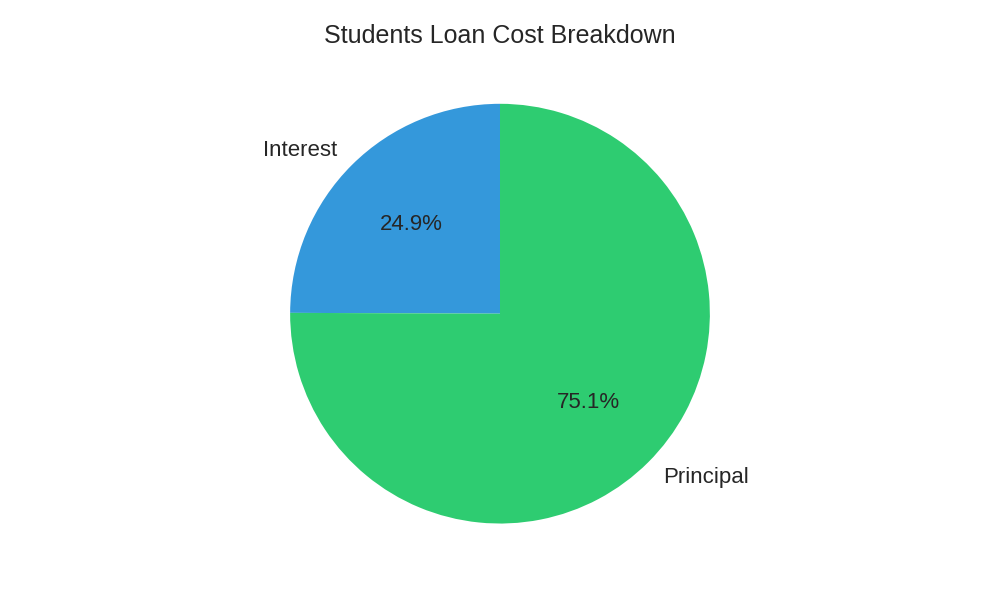

Let’s illustrate with an example. If you borrow $30,000 for a student loan at a fixed annual interest rate of 6% over a 10-year repayment term, your monthly payment would be approximately $333.06. Over the life of this loan, you would pay back a total of $39,967.20, meaning the total interest paid would be $9,967.20.

Here’s a simplified repayment schedule to show how your principal balance decreases over time, assuming a consistent monthly payment:

| Year | Remaining Principal (approx.) | Monthly Payment |

|---|---|---|

| 0 (Initial) | $30,000.00 | N/A |

| 1 | $27,448.52 | $333.06 |

| 5 | $16,722.47 | $333.06 |

| 10 | $0.00 | $333.06 |

Monthly Payment Calculator

Repayment Strategies and Managing Debt

Once you graduate, repayment begins. Having a solid strategy can make a significant difference in managing your **student loan** debt.

Federal Loan Repayment Options

Federal loans offer several flexible repayment plans:

- Standard Repayment Plan: Fixed monthly payments for up to 10 years (or 30 years for consolidated loans). This typically results in the least amount paid in interest over time.

- Graduated Repayment Plan: Payments start low and increase every two years, usually over a 10-year period.

- Extended Repayment Plan: Payments are fixed or graduated for up to 25 years, often resulting in lower monthly payments but more interest paid overall.

- Income-Driven Repayment (IDR) Plans: Payments are capped at a percentage of your discretionary income and recalculated annually. Examples include REPAYE, PAYE, IBR, and ICR. These plans can lead to loan forgiveness after 20-25 years of payments.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.