You’re standing on the precipice of one of life’s biggest decisions: buying a home. Exciting, terrifying, and loaded with questions. The biggest one echoing in your mind is probably, “how much mortgage can I afford?” It’s a question that keeps countless prospective homeowners up at night, and frankly, the answers you get from lenders might not be the whole truth. They’ll tell you what they can lend, but rarely what you can comfortably afford. This isn’t just about qualifying for a loan; it’s about securing your financial future. If you’re wondering how much mortgage can I afford without sacrificing your entire lifestyle, you’re in the right place.

I’m here to cut through the noise, empower you with insider knowledge, and help you make a confident, financially sound decision today. Forget the generic advice; we’re diving deep into what truly impacts your wallet.

Beyond the “Pre-Approved” Illusion: Your Real Affordability

Here’s a hard truth: the amount a bank pre-approves you for is often the maximum loan limit they’re willing to give, not what you should actually spend. This is a common pitfall that leaves many prospective homeowners feeling “house poor.” You need to understand that your comfortable budget and the lender’s limit are two very different numbers.

Insider Tip: Lender pre-approvals are NOT your personal budget. They are based on rigid formulas that don’t account for your specific lifestyle, your daily coffee habit, or your child’s extracurricular activities. They often overlook the unexpected costs that pop up in homeownership.

Imagine you’re a young couple, both earning a solid income, pre-approved for a $400,000 mortgage. Thrilled, you start looking at homes in that price range. But what the lender didn’t factor in are your plans for a big family vacation every year, your student loan payments that still feel heavy, or your desire to save aggressively for retirement. If you take that full $400,000, suddenly, those other financial goals become impossible. This matters in real life because it prevents you from making a decision you’ll regret years down the line.

The Core Pillars of Your True Budget

Before you even look at a house, look inward at these fundamental financial pillars. They are the bedrock of your personal affordability equation.

-

Income Stability: It’s not just about how much you make, but how reliably you make it. Lenders love consistent W2 income, but if you’re self-employed, they’ll want two years of tax returns. For you, it means evaluating if your income is likely to stay the same, or even grow, over the next few years. Predictable income means predictable payments.

-

Debt-to-Income (DTI) Ratio: This is a critical metric for lenders, but it should be even more critical for you. Your DTI is the percentage of your gross monthly income that goes towards debt payments (credit cards, student loans, car loans, and your future mortgage payment). While lenders might approve you up to a 43-50% DTI, pushing that limit means less financial flexibility. Aim for a DTI below 36% for maximum comfort.

-

Credit Score: Your credit score is more than just a number; it’s your financial reputation. A higher score means you’re seen as a less risky borrower, which translates into lower interest rates on your mortgage. Even a half-point difference in interest can save you tens of thousands of dollars over the life of the loan. You can learn more about managing your credit from resources like the Consumer Financial Protection Bureau.

Common Myth to Avoid: Thinking a perfect credit score guarantees the lowest rate without looking at other factors. While a great credit score is essential, it’s just one piece of the puzzle. Lenders also scrutinize your income, debt, and the specific loan product you choose. Don’t assume a high score means you’re immune to other financial constraints.

Deconstructing the Monthly Payment: It’s More Than P&I

When you get a mortgage quote, the lender often focuses on the Principal and Interest (P&I) payment. But your actual monthly housing expense is almost always higher. You need to factor in the full picture to understand your true commitment.

Pro/Con Analysis: A low interest rate is fantastic, but if the property you’re eyeing has sky-high property taxes, your monthly payment might still be unaffordable. Conversely, a slightly higher interest rate on a property with low taxes and no HOA could be a better deal for your budget.

Your full monthly payment is often referred to as PITI: Principal, Interest, Taxes, and Insurance.

- Principal: The portion of your payment that goes towards paying down the actual loan amount.

- Interest: The cost of borrowing the money.

- Taxes: Your annual property taxes, usually divided by 12 and collected monthly by your lender into an escrow account.

- Insurance: Your homeowner’s insurance premium, also typically collected monthly into escrow.

Insider Tip: Don’t forget HOA fees, Private Mortgage Insurance (PMI), and maintenance costs. If your down payment is less than 20%, you’ll likely pay PMI, which is an extra monthly charge that protects the lender. Many homes, especially condos or those in planned communities, also have Homeowners Association (HOA) fees. And remember, homes require maintenance! Budget at least 1-3% of the home’s value annually for repairs and upkeep. Imagine two identical houses, both listed at $350,000. House A has $2,500 in annual property taxes and no HOA. House B has $6,000 in annual property taxes and a $250 monthly HOA fee. While their listing price is the same, House B will have a significantly higher monthly housing cost, making it less affordable despite the identical price tag. This matters because neglecting these “hidden” costs leads to financial stress and buyer’s remorse.

Practical Guide: How Much Mortgage Can You Truly Afford?

Let’s get practical. Figuring out how much mortgage can I afford isn’t rocket science, but it requires honesty with yourself. This isn’t about what a bank thinks you can handle; it’s about what you know you can handle without feeling squeezed.

The infamous 28/36 Rule is a good starting point, but understand its true meaning for YOU. This rule suggests that your housing costs (PITI + HOA) shouldn’t exceed 28% of your gross monthly income, and your total debt payments (housing + all other debts) shouldn’t exceed 36% of your gross monthly income. This rule is a guideline for lenders, but for consumer comfort, aiming below these percentages is always wise. It gives you a buffer for life’s unexpected events.

To really calculate your comfort level:

-

Calculate Your True Monthly Income: Use your net (take-home) pay, not gross. This is the money you actually have to spend.

-

List All Current Monthly Expenses: Every single one – rent, car payments, student loans, credit card minimums, groceries, utilities, subscriptions, entertainment, savings contributions. Be brutally honest.

-

Determine Your ‘Comfortable’ Surplus: Subtract your total expenses from your net income. This is your discretionary income. A portion of this will need to go towards your mortgage payment.

-

Estimate PITI + Other Costs: For a potential home, get estimates for property taxes and homeowner’s insurance. Factor in potential HOA fees and an estimate for PMI if your down payment is under 20%. Don’t forget that maintenance buffer.

-

Work Backward: See what mortgage principal and interest payment you can comfortably fit into your budget after all other housing costs and your desired savings/discretionary spending are accounted for. This gives you a clear picture of what loan amount truly fits your lifestyle.

Unlock how much mortgage you can truly afford

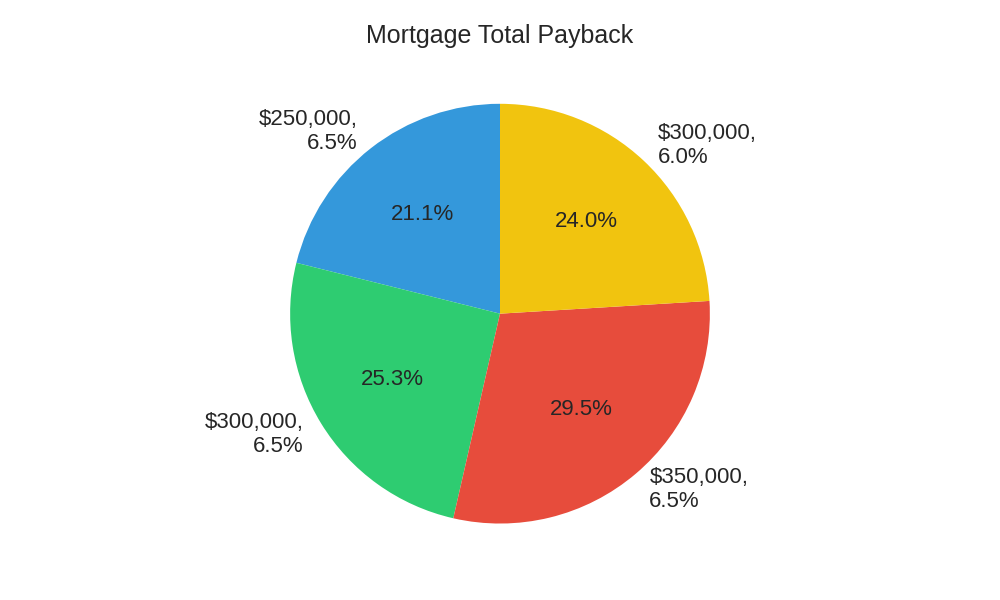

To illustrate the long-term impact of even small differences, let’s look at a Total Cost Analysis for varying loan amounts and interest rates. These are illustrative figures, and actual costs will depend on specific loan terms and market rates. Always consult with a financial advisor for personalized advice.

| Loan Amount (Example) | Interest Rate (Example) | Estimated Monthly P&I | Total Interest Paid (30 yrs) | Total Payback (30 yrs, P&I) |

|---|---|---|---|---|

| $250,000 | 6.5% | $1,580 | $318,800 | $568,800 |

| $300,000 | 6.5% | $1,896 | $382,500 | $682,500 |

| $350,000 | 6.5% | $2,212 | $446,200 | $796,200 |

| $300,000 | 6.0% | $1,799 | $347,700 | $647,700 |

As you can see, even a slightly higher interest rate or loan amount dramatically increases the total cost over 30 years. This table highlights why understanding your total payback is far more important than just the monthly payment when considering affordability.

The Down Payment Dilemma & Emergency Fund Imperative

The down payment is often the biggest hurdle to homeownership. You’ve heard the advice: “Save 20% to avoid PMI!” While this is sound advice, it’s not always feasible or the best immediate strategy for everyone.

Common Myth to Avoid: Waiting for 20% down is always the best strategy. For some, waiting years to save 20% means missing out on potential home appreciation, especially in rising markets. Loans like FHA or conventional loans with lower down payment options can get you into a home sooner. The trade-off is often PMI, but that can sometimes be removed later or offset by property value gains.

However, what you absolutely cannot compromise on is an emergency fund. Even if you put down a lower down payment, you need a robust savings account. Imagine a family that scraped together every penny for a 20% down payment, leaving them with just a few hundred dollars in their checking account. Two months after moving in, the furnace dies, costing $5,000 to replace. Without an emergency fund, they’re suddenly facing high-interest debt just to keep their home warm. This is why you need accessible cash; for unexpected repairs, job loss, or medical emergencies.

Before closing, you’ll also have closing costs – fees for appraisals, inspections, title insurance, and more. These can range from 2-5% of the loan amount. Make sure you have these funds readily available, separate from your down payment and emergency savings. Consulting resources like The Wall Street Journal can provide insights into current market conditions and costs.

Conclusion: Your Empowered Decision

Understanding how much mortgage can I afford is less about a lender’s formula and more about your personal financial reality. It’s about being honest with your budget, anticipating future costs, and prioritizing your long-term financial health. You are now equipped with the insider tips and critical thinking to truly unlock your homeownership potential.

Don’t let the excitement of a new home blind you to the numbers. Take control of your financial future, starting now. Analyze your budget, understand all the costs involved, and prioritize building that emergency fund. If you’re unsure, reach out to a trusted, independent financial advisor who can provide tailored guidance, not just try to sell you a loan. Get started today by reviewing your finances with a fine-tooth comb. Your future self will thank you for making an informed, confident decision.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.