When you’re facing unexpected expenses, a pressing financial need, or simply want to consolidate existing debt, a personal loan can be a crucial lifeline. However, if your credit score isn’t where you want it to be, the idea of getting a personal loan approval might seem like an insurmountable challenge. Many people believe that poor credit automatically disqualifies them from accessing necessary funds, leading to frustration and continued financial stress.

You might feel trapped, constantly rejected by traditional lenders, or worried about being exploited by predatory loans with sky-high interest rates. This article is designed to empower you by debunking common myths and providing a clear, actionable roadmap to securing a personal loan, even when your credit history has a few bumps. We’ll explore genuine strategies, clarify what lenders look for beyond just a credit score, and help you navigate the process with confidence.

Understanding Your Credit and Its Impact

Before diving into solutions, it’s essential to understand why your credit score matters and how it influences lenders’ decisions. Your credit score is a numerical representation of your creditworthiness, essentially a report card on how reliably you’ve managed debt in the past. Lenders use it to assess the risk of lending money to you. A lower score often signals a higher risk, which can lead to denials or significantly higher interest rates.

The Reality of Bad Credit Lending

It’s a common misconception that lenders only approve applicants with excellent credit. While a strong credit score certainly opens more doors, many lenders specialize in offering personal loans to individuals with less-than-perfect credit. These lenders understand that life happens, and past financial difficulties shouldn’t permanently shut you out of opportunities. The key is knowing where to look and what steps to take to make yourself a more attractive borrower.

- Payment History: This is the most significant factor, showing if you pay bills on time.

- Credit Utilization: How much credit you’re using compared to your available credit limit. Keeping this low is crucial.

- Length of Credit History: A longer history of responsible credit use is generally better.

- Credit Mix: Having a variety of credit accounts (e.g., credit cards, auto loans) can be beneficial.

- New Credit: Applying for too much new credit in a short period can temporarily lower your score.

Strategies to Improve Your Chances of Personal Loan Approval

Even with poor credit, there are concrete steps you can take to strengthen your application and increase your likelihood of approval. These strategies focus on demonstrating your ability and willingness to repay the loan, going beyond just your raw credit score.

1. Check Your Credit Report and Dispute Errors

The first step is always to know exactly where you stand. Obtain a copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion). Review it meticulously for any errors, such as incorrect late payments, accounts you don’t recognize, or incorrect balances. Disputing and correcting these errors can often lead to a quick boost in your credit score, making a real difference in loan eligibility and rates.

2. Secure a Co-signer

If you have a trusted friend or family member with good credit, asking them to co-sign your personal loan application can significantly improve your chances. A co-signer agrees to be legally responsible for the loan if you fail to make payments. This reduces the risk for the lender, as they have another party to pursue for repayment. However, ensure both you and your co-signer understand the implications, as their credit will also be affected if you miss payments.

3. Explore Secured Personal Loans

A secured personal loan involves pledging an asset as collateral. This could be a car, savings account, or certificate of deposit (CD). By providing collateral, you reduce the lender’s risk, making them more willing to approve your application, even with poor credit. Secured loans often come with lower interest rates compared to unsecured options because of the reduced risk. Just be aware that if you default, you could lose your collateral.

4. Demonstrate Stable Income and Employment

Lenders want to see that you have a reliable source of income to repay the loan. Even if your credit score is low, a consistent employment history and steady income can be a strong compensating factor. Be prepared to provide pay stubs, bank statements, and employment verification to prove your financial stability. This helps assure lenders that you have the cash flow to handle new debt obligations.

5. Lower Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is a crucial metric for lenders. It compares your total monthly debt payments to your gross monthly income. A high DTI indicates that a large portion of your income is already committed to existing debts, making you a higher risk for new loans. Prioritize paying down existing debts, especially those with high interest rates, before applying for a new personal loan. Reducing your DTI shows lenders you have more disposable income to manage new payments.

Where to Find Personal Loans for Bad Credit

Not all lenders are created equal, especially when it comes to serving borrowers with poor credit. Knowing where to focus your search can save you time and frustration.

Online Lenders

Many online lenders specialize in bad credit loans and often have more flexible underwriting criteria than traditional banks. They can process applications quickly and offer competitive rates for their target market. Research reputable online platforms and read reviews to find lenders known for working with various credit profiles. Sites like NerdWallet or Bankrate can provide comparisons and reviews of various lenders.

Credit Unions

Credit unions are member-owned financial institutions that often have a more community-focused approach. They may be more willing to work with members who have lower credit scores, especially if you have an existing relationship with them. Their interest rates can also be more favorable than those from for-profit banks. Consider joining a local credit union and discussing your options.

Banks with Existing Relationships

If you’ve been a long-time customer with a particular bank, they might be more inclined to approve a personal loan application, even if your credit isn’t perfect. Your history with them, including how you manage your checking and savings accounts, can serve as an alternative indicator of your financial responsibility. It’s always worth speaking to a loan officer at your current bank.

Calculating Your Potential Personal Loan Payments

Understanding the financial commitment of a personal loan is crucial before you apply. Even with bad credit, lenders are required to disclose all terms, including interest rates and fees. You need to calculate not just the monthly payment but also the total cost of the loan over its lifetime, including all interest.

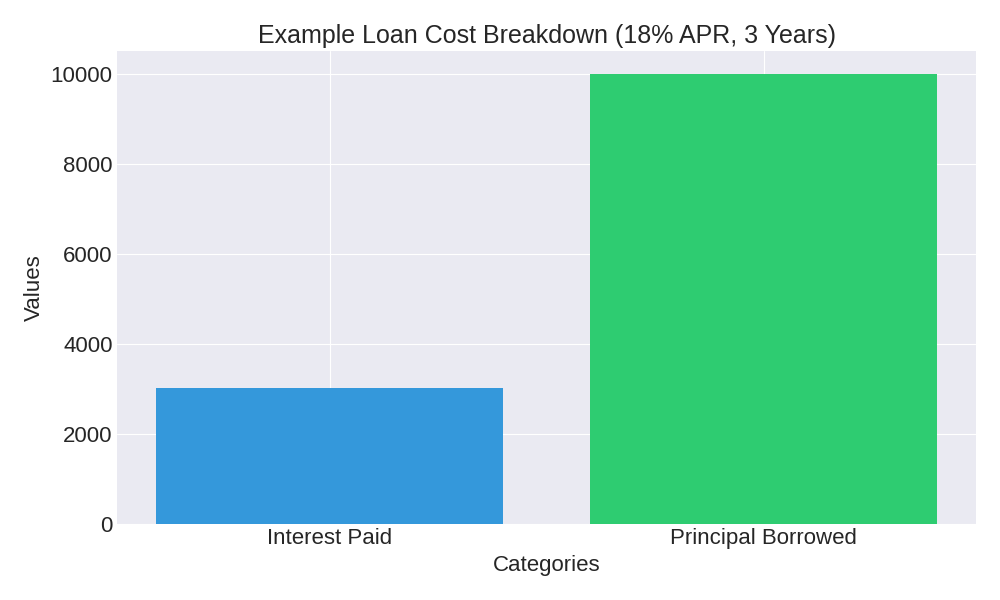

Let’s consider an example: You need a personal loan of $10,000, and given your credit situation, you might be offered an Annual Percentage Rate (APR) of 18%. The repayment term will significantly impact your monthly payment and the total interest you pay.

| Loan Term (APR: 18%) | Approx. Monthly Payment | Approx. Total Interest Paid |

|---|---|---|

| 3 Years (36 Months) | $361.52 | $3,014.72 |

| 5 Years (60 Months) | $253.93 | $5,235.80 |

Monthly Payment Calculator

As you can see from the table, a longer loan term (like 5 years) reduces your monthly payment, making it more manageable. However, it also significantly increases the total interest you’ll pay over the life of the loan. This is a critical trade-off to consider: lower monthly payments often mean a higher overall cost. Always aim for the shortest term you can comfortably afford to minimize interest expenses.

Building Better Credit for the Future

Securing a personal loan with poor credit is a step forward, but it’s also an opportunity to start building a stronger financial future. Making your loan payments on time and in full is one of the most effective ways to improve your payment history and, consequently, your credit score. Over time, demonstrating responsible repayment will open doors to better loan offers and lower interest rates for future borrowing needs.

- Pay Bills on Time: Set up reminders or automatic payments to avoid missing due dates.

- Keep Credit Utilization Low: Aim to use no more than 30% of your available credit on credit cards.

- Avoid Unnecessary New Credit: Don’t open multiple new credit accounts in a short period.

- Monitor Your Credit Regularly: Keep an eye on your credit report for any changes or potential fraud.

Conclusion: Your Path to Financial Empowerment

Getting a personal loan with poor credit doesn’t have to be an impossible dream. By understanding your current financial standing, actively working to improve your creditworthiness, exploring the right lenders, and carefully calculating the true cost of borrowing, you can unlock the financial resources you need. Remember, patience and persistence are key. Every responsible financial decision you make, including timely personal loan repayments, contributes to building a stronger financial future.

Don’t let past credit challenges define your future opportunities. Take the first step today: check your credit report, explore your options, and confidently pursue the financial solutions that empower you. You have the power to change your financial narrative.

Ready to explore your options? Start by checking your credit score and researching lenders that specialize in bad-credit personal loans. Compare interest rates, terms, and fees carefully before making a decision. Focus on solutions that align with your budget and long-term goals, not just immediate needs. Taking informed action today can reduce financial stress and create lasting stability. With the right approach, this loan can become a stepping stone toward greater financial confidence and control.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.