You’re paying rent every month, diligently keeping a roof over your head. You probably think your landlord’s insurance policy covers everything inside, right? Or perhaps you believe your old laptop and hand-me-down sofa aren’t valuable enough to insure. This mindset leaves you dangerously exposed. Ignoring the critical need for insurance for renters is a financial gamble you absolutely cannot afford to take, especially when disasters strike unexpectedly.

In a world where unforeseen events can turn your life upside down in an instant, having robust insurance for renters isn’t a luxury; it’s a fundamental safeguard. You need to make a decision now, not later, because waiting could cost you everything. Let’s cut through the noise and expose why this coverage is indispensable for your financial security.

Why Your Landlord’s Policy Isn’t Your Safety Net

One of the biggest misconceptions we see is the belief that your landlord’s insurance policy offers you protection. It doesn’t. Your landlord’s policy covers the building itself – the walls, the roof, the appliances they own. It absolutely does not cover your personal belongings or protect you from liability if someone gets hurt in your rented space.

Imagine this scenario: You’re living in an apartment, and a pipe bursts upstairs, flooding your unit. Your landlord’s policy might pay to repair the damaged walls and floors of the building. But what about your ruined electronics, furniture, clothes, and sentimental items? Those are your responsibility to replace. Without renters insurance, you’re looking at thousands of dollars out of your own pocket to rebuild your life.

This is precisely why you need your own specific coverage. It protects what is uniquely yours, providing a crucial financial buffer against the unexpected.

The Real Costs of “It Won’t Happen to Me”

Many renters dismiss insurance because they think the risks are low. They believe theft, fire, or accidental damage only happen to “other people.” This denial is financially perilous. The actual cost of replacing everything you own, or facing a lawsuit, far outweighs the modest premium of a renters policy.

Consider a mini case study: Sarah lives in a one-bedroom apartment. Her landlord’s building suffers a kitchen fire, rendering her unit unlivable for three months. All her furniture, clothes, and electronics are smoke-damaged beyond repair. Without renters insurance, Sarah would not only have to find money for a temporary place to stay (hotel, food, laundry) but also save up anywhere from $10,000 to $30,000 to replace her personal property. With a good renters policy, she’d likely pay a small deductible, and the insurer would cover her temporary living expenses and the replacement cost of her belongings.

Beyond Your Stuff: The Critical Role of Liability Coverage

While protecting your belongings is vital, the liability component of insurance for renters is often the most overlooked – and potentially the most financially devastating if you lack it. This coverage protects you financially if you accidentally cause injury to someone or damage someone else’s property, either in your home or elsewhere.

Why this matters in real life: Let’s say a friend slips on a wet floor in your kitchen and breaks their arm. Or perhaps your bathtub overflows, causing significant water damage to the apartment below you. Without liability coverage, you could be personally responsible for their medical bills, lost wages, and property repair costs. These expenses can easily spiral into tens or even hundreds of thousands of dollars, leading to severe financial hardship or even bankruptcy.

Your renters insurance steps in to cover these legal and medical costs, often up to significant limits, shielding your assets from catastrophic claims. To understand more about liability insurance in general, you can visit a trusted resource like the National Association of Insurance Commissioners.

Common Myths to Avoid When Considering Renters Insurance

Don’t fall for these widespread misconceptions that can leave you vulnerable:

- Myth #1: My belongings aren’t worth much. Most people underestimate the value of their possessions until they need to replace everything. From clothes and shoes to kitchenware, books, and electronics, the total cost adds up rapidly. Even a modest apartment can hold $15,000 to $25,000 worth of belongings.

- Myth #2: It’s too expensive. Renters insurance is surprisingly affordable, often costing less than your daily coffee habit. Many policies range from $15 to $30 per month, a small price for significant peace of mind.

- Myth #3: It only covers theft. While theft is a key component, renters insurance typically covers a wide range of perils, including fire, smoke, certain water damage (like burst pipes, not floods unless specified), windstorms, and vandalism.

Insider Tips for Maximizing Your Renters Insurance Value

As a consumer advocate, I can tell you that smart shopping can save you money and get you better coverage:

- Bundle Your Policies: Often, you can get a discount by bundling your renters insurance with your auto insurance policy from the same provider. Always ask for bundling options.

- Choose the Right Deductible: A deductible is the amount you pay out-of-pocket before your insurance kicks in. A higher deductible usually means a lower monthly premium, but ensure it’s an amount you can comfortably afford in an emergency.

- Take Inventory: Create a detailed home inventory of your belongings. Take photos or videos, list serial numbers, and keep receipts for expensive items. This makes filing a claim much smoother. There are apps specifically designed for this.

-

Understand Replacement Cost vs. Actual Cash Value:

- Replacement Cost Value (RCV): Pays to replace your damaged property with new items, without deducting for depreciation. This is generally the superior option.

- Actual Cash Value (ACV): Pays for the depreciated value of your items. An old TV might only get you a fraction of its original cost.

Always opt for RCV if your budget allows.

- Review Coverage Limits: Don’t just settle for the lowest premium. Ensure your personal property limit adequately covers the estimated value of your belongings. Also, verify your liability limits are robust enough for your peace of mind. A common recommendation is at least $100,000 in liability coverage.

Understanding Your Coverage: What’s Truly Protected?

Renters insurance typically breaks down into three core areas:

- Personal Property Coverage: This protects your personal belongings from covered perils. This includes everything you own, from your toothbrush to your television, whether it’s stolen, damaged by fire, or ruined by a burst pipe.

- Liability Coverage: This is your shield against lawsuits. If someone is injured in your apartment, or you accidentally damage someone else’s property, your policy can cover legal fees, medical expenses, and settlement costs up to your policy limits.

- Additional Living Expenses (ALE) / Loss of Use: If a covered event makes your rental uninhabitable, ALE covers the additional costs you incur while your home is being repaired. This can include hotel stays, temporary rent, restaurant meals above your usual budget, and even laundry services.

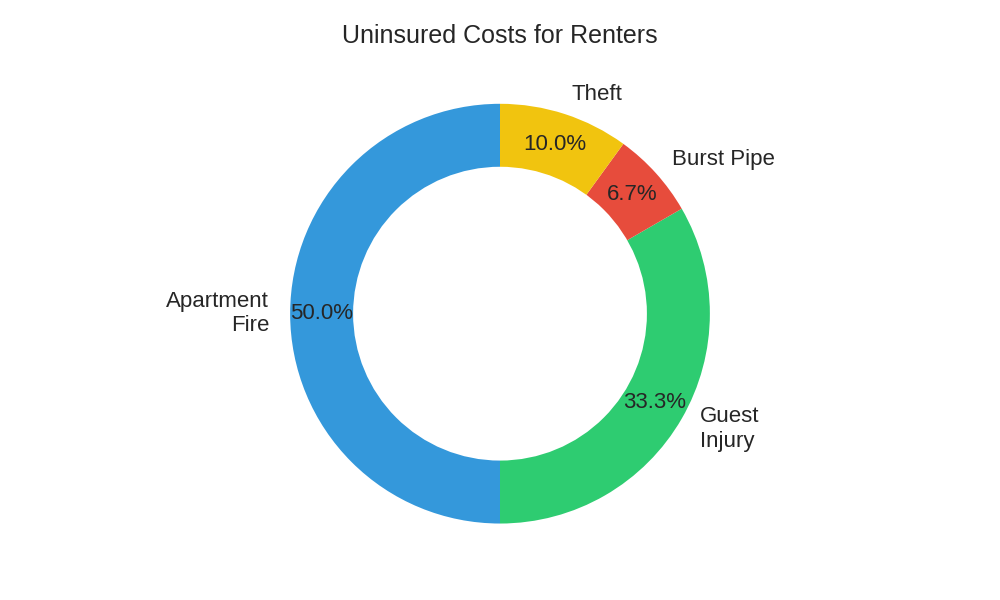

To illustrate the stark difference, let’s look at a potential incident:

| Incident Type | Cost Without Renters Insurance (Estimated Range) | Cost With Renters Insurance ($500 Deductible) |

|---|---|---|

| Apartment Fire (Property Damage) | $15,000 – $30,000+ (replace all belongings) | $500 (deductible) |

| Guest Injury (Medical & Legal) | $10,000 – $100,000+ (medical bills, lawsuit) | $500 (deductible) |

| Burst Pipe (Temp Housing) | $2,000 – $5,000 (3 weeks hotel, food) | $500 (deductible) |

| Theft (High-value items) | $3,000 – $10,000 (replace electronics, jewelry) | $500 (deductible) |

As you can clearly see, even with a deductible, the financial relief provided by renters insurance is monumental compared to facing these costs alone. For more detailed information on policy coverages, you might find valuable insights at Investopedia.

How to Calculate Your Coverage Needs

Estimating how much renters insurance you need doesn’t require advanced math, just a careful look at your life. Here’s a practical approach:

Personal Property Coverage

Walk through your entire home, room by room, and list every significant item. For each item, estimate its replacement cost if it were brand new today. Don’t think about what you paid for it years ago; think about what it would cost to buy a new equivalent. You’d be surprised how quickly those numbers add up.

For example, a living room might have a sofa ($1,000), a TV ($500), a coffee table ($200), lamps ($150), and various decorative items ($300). Add in your bedroom furniture, clothing, kitchenware, and all your electronics. Most people find their total possessions are worth at least $15,000 to $25,000, and often much more. This is the minimum personal property coverage you should aim for.

Liability Coverage

For liability, consider your assets. If you were sued, how much are you trying to protect? Many financial advisors recommend at least $100,000 to $300,000 in liability coverage. This helps safeguard your savings and future earnings from potential lawsuits. The cost difference between $100,000 and $300,000 in liability coverage is often minimal, making the higher limit a smart choice.

Additional Living Expenses

Estimate how much it would cost you per month to live elsewhere if your apartment became unlivable. Think about hotel costs, food, and other incidentals. Most policies offer limits between 20-30% of your personal property coverage, which is typically sufficient. A good rule of thumb is to have enough coverage to cover 3-6 months of temporary living expenses.

It’s important to remember these are estimates to guide your decision. When in doubt, err on the side of slightly more coverage rather than less. You can also consult an insurance agent to help tailor a policy to your specific needs.

Renters Insurance Value Calculator

The Time to Act is Now

Procrastination here is a luxury you simply cannot afford. Every day you rent without insurance for renters, you are gambling with your financial stability. The small monthly premium is a tiny investment for the enormous peace of mind and financial protection it provides.

Don’t wait for a flood, fire, or theft to realize the crucial value of this coverage. Be proactive, protect your assets, and secure your financial future. You owe it to yourself to be prepared.

Ready to Protect Your Future?

Call to Action: Don’t delay. Take the first step towards securing your assets today. Get a free renters insurance quote and compare options tailored to your needs. It takes only a few minutes, and it could save you from catastrophic financial loss.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.