Welcome to your essential guide for mastering your financial future through strategic investing. In today’s dynamic financial landscape, understanding how to leverage an investing bank or its investment services is paramount. This comprehensive guide will simplify complex concepts, providing you with actionable steps to build and secure your wealth. We believe that everyone deserves the knowledge to make informed financial decisions, turning aspirations into reality.

Whether you’re new to the world of finance or looking to refine your strategy, this article cuts through the jargon. It empowers you to understand the potential of your money, offering clear pathways to growth. By engaging with an investing bank, you can access a spectrum of tools and expertise designed to help your capital work harder for you. Let’s unlock the secrets to a prosperous financial journey together.

Understanding Your Financial Goals

Before you commit any capital, defining what you want your money to achieve is the first, most critical step. Your financial goals will dictate your investment strategy, guiding your choices of investment vehicles and risk levels.

Short-term vs. Long-term Objectives

Short-term goals typically involve objectives within the next 1-5 years, such as saving for a down payment on a house, a new car, or a significant vacation. For these, investments with lower volatility and easier access are usually preferred. Conversely, long-term goals extend beyond five years, encompassing aspirations like retirement planning, funding a child’s education, or building substantial wealth. These goals often benefit from investments with higher growth potential, even if they carry more risk over shorter periods.

Assessing Your Risk Tolerance

Risk tolerance is your comfort level with potential fluctuations in your investment’s value. Are you comfortable seeing your investments drop significantly in value for the potential of higher returns, or do you prefer a more stable, albeit slower, growth path? Understanding this is crucial for selecting appropriate investment products. A lower risk tolerance might lead you towards more conservative assets, while a higher tolerance could open doors to more aggressive, growth-oriented investments.

Core Investment Vehicles Explained

Navigating the various investment options can seem daunting, but at their core, they serve distinct purposes in your portfolio. An effective investing bank will offer a range of these to suit diverse needs.

Stocks: Ownership in Companies

When you buy a stock, you’re purchasing a small piece of ownership in a public company. As the company grows and profits, the value of your stock can increase, and you might also receive dividends (a portion of the company’s earnings). Stocks are generally considered growth-oriented investments, carrying higher risk but also higher potential returns.

Bonds: Lending to Governments or Corporations

Bonds represent a loan made by an investor to a borrower, such as a government or a corporation. In return, the borrower promises to pay regular interest payments over a specified period and return the original principal amount at maturity. Bonds are generally considered less risky than stocks and provide a steady income stream, making them a crucial component for portfolio diversification. Learn more about different types of investments and their characteristics at Investor.gov.

Mutual Funds & ETFs: Diversified Baskets

Mutual funds and Exchange Traded Funds (ETFs) allow you to invest in a diversified portfolio of stocks, bonds, or other assets with a single purchase. A mutual fund is professionally managed, while an ETF often tracks a specific index (like the S&P 500) and can be traded throughout the day like a stock. They offer instant diversification, reducing the risk associated with investing in individual securities.

Building Your Investment Strategy

A well-defined investment strategy is your roadmap to financial success. It should align with your goals and risk tolerance, providing a structured approach to your investments.

The Power of Diversification

Diversification is the strategy of spreading your investments across various asset classes, industries, and geographies. The principle is simple: don’t put all your eggs in one basket. If one investment performs poorly, others might perform well, balancing your overall portfolio and mitigating risk. It’s a fundamental principle for long-term investing success.

Dollar-Cost Averaging: Smoothing Out Volatility

Dollar-cost averaging (DCA) involves investing a fixed amount of money at regular intervals, regardless of market fluctuations. This strategy helps reduce the impact of market volatility. When prices are high, your fixed amount buys fewer shares; when prices are low, it buys more. Over time, this averages out your purchase price and can lead to better returns than trying to time the market.

Portfolio Rebalancing: Staying on Track

Portfolio rebalancing is the process of adjusting your portfolio periodically to maintain your desired asset allocation. For instance, if stocks have performed exceptionally well, they might now represent a larger percentage of your portfolio than you initially intended. Rebalancing involves selling some of your outperforming assets and buying more of the underperforming ones, bringing your portfolio back to its target allocation and risk level.

The Power of Compounding: How Your Money Grows

Compounding is often called the “eighth wonder of the world” because it allows your investments to grow exponentially over time. It’s the process where the returns you earn on your initial investment also start earning returns, leading to a snowball effect.

How to Calculate Compound Growth (Plain Language)

Imagine you invest $1,000, and it earns a 10% return in the first year. Your investment grows to $1,100. In the second year, you don’t just earn 10% on your original $1,000; you earn 10% on the new total of $1,100. This means you earn $110, bringing your total to $1,210. Each year, your earnings grow larger because they’re based on an ever-increasing principal amount. This cycle of earning returns on your returns is the magic of compounding.

Monthly Payment Calculator

The earlier you start, the more time your money has to compound, leading to significant wealth accumulation over decades. Even small, consistent contributions can lead to substantial sums thanks to this powerful effect.

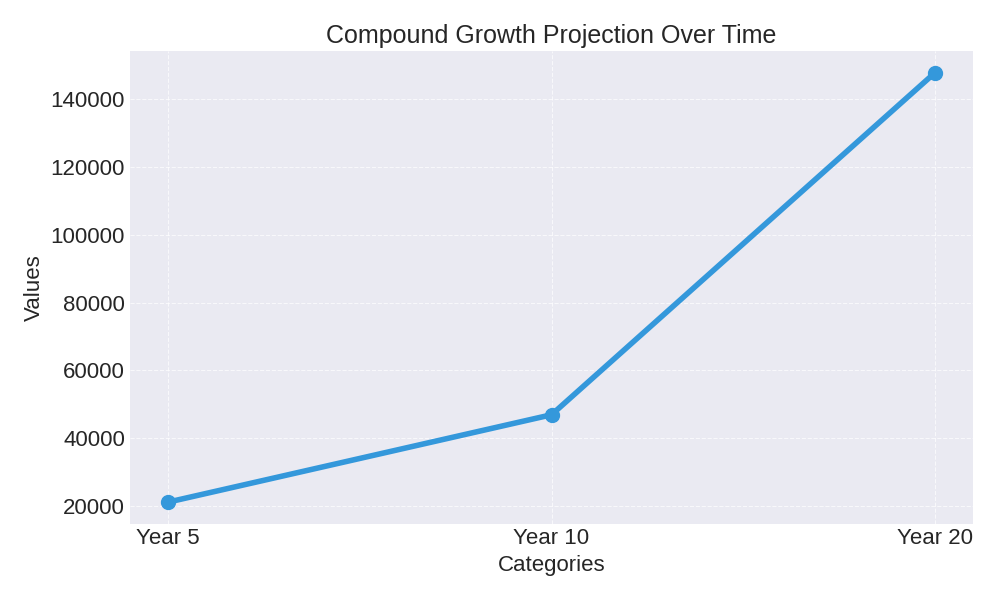

Compound Growth Scenario: Long-Term Value

Let’s illustrate the impact of consistent investment and compounding over different time horizons, assuming an initial investment of $5,000 and an additional $200 contributed monthly, with an average annual return of 7%.

| Investment Period | Total Invested | Projected Value |

|---|---|---|

| Year 5 | $17,000 | $21,173 |

| Year 10 | $29,000 | $46,929 |

| Year 20 | $53,000 | $147,750 |

Choosing the Right ‘Investing Bank’ Partner

Selecting the right financial institution is crucial for your investment journey. Look for a partner that aligns with your needs, offers competitive services, and provides robust support.

Types of Institutions and Services

You have several options: traditional banks often have investment divisions, dedicated brokerage firms specialize in trading, and robo-advisors offer automated, low-cost investment management. Each has its pros and cons regarding fees, human interaction, and available investment products. Consider whether you prefer a hands-on approach, professional guidance, or a fully automated solution.

Fees and Transparency

Always understand the fee structure. These can include management fees, trading commissions, advisory fees, and expense ratios for funds. High fees can significantly erode your returns over time. Look for institutions that are transparent about all costs associated with their services. For guidance on choosing financial professionals and understanding their duties, visit FINRA.org.

Navigating Risks and Protecting Your Investments

Investing always involves some level of risk. Understanding these risks and how to mitigate them is crucial for protecting your financial well-being.

Market Volatility and Inflation

Market volatility refers to the ups and downs of asset prices, which are a normal part of investing. While it can be unsettling, a long-term perspective and diversification help to ride out these fluctuations. Inflation, the gradual increase in prices over time, erodes the purchasing power of your money. Your investments need to grow at a rate higher than inflation to genuinely increase your wealth.

Fraud and Investor Protection

Be vigilant against investment fraud. Always deal with reputable firms and verify their credentials. In the United States, institutions like the Securities Investor Protection Corporation (SIPC) protect investors against the loss of cash and securities held by a failed brokerage firm. The U.S. Securities and Exchange Commission (SEC) also works to protect investors and maintain fair markets. Learn more about investor protection and avoiding fraud at SEC.gov.

Frequently Asked Questions (FAQ)

-

What’s the minimum amount to start investing?

Many platforms allow you to start with very little, sometimes as low as $5 or $10 through fractional shares or micro-investing apps. Mutual funds might have minimums, but ETFs generally do not. The most important thing is to start, even if it’s a small amount, and be consistent.

-

How often should I check my investments?

For long-term investors, constantly checking your portfolio can lead to impulsive decisions based on short-term market noise. A quarterly or semi-annual review is often sufficient to rebalance and ensure your strategy still aligns with your goals. Avoid daily monitoring.

-

Should I pay off debt or invest?

This depends on the interest rate of your debt. If you have high-interest debt, like credit card debt, paying it off usually offers a guaranteed “return” (by saving on interest) that often outweighs potential investment returns. For lower-interest debt, like a mortgage, investing might be a better option, but it’s a personal decision requiring careful consideration of your financial situation.

-

Is my money safe in an investing bank?

Reputable investing banks are heavily regulated. Investment accounts in the U.S. are often protected by SIPC for up to $500,000 (including $250,000 for cash) against brokerage firm failure, though this doesn’t protect against market losses. Always ensure your chosen institution is legitimate and regulated.

Conclusion

Mastering your money and securing your future is an achievable goal for everyone. By understanding your financial goals, choosing appropriate investment vehicles, building a sound strategy, and leveraging the power of compounding, you lay the groundwork for lasting wealth. An investing bank, or its investment services, can be a vital partner in this journey, providing the tools and expertise you need.

Remember, the most crucial step is to start. Educate yourself, make informed decisions, and stay consistent. Your financial future is in your hands, and with this guide, you have the knowledge to take control.

Ready to Secure Your Future?

Begin by assessing your current financial situation and setting clear, actionable goals. Consider reaching out to a qualified financial advisor to help tailor a strategy that perfectly fits your unique circumstances. The sooner you start, the more profound the impact of your efforts will be.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.